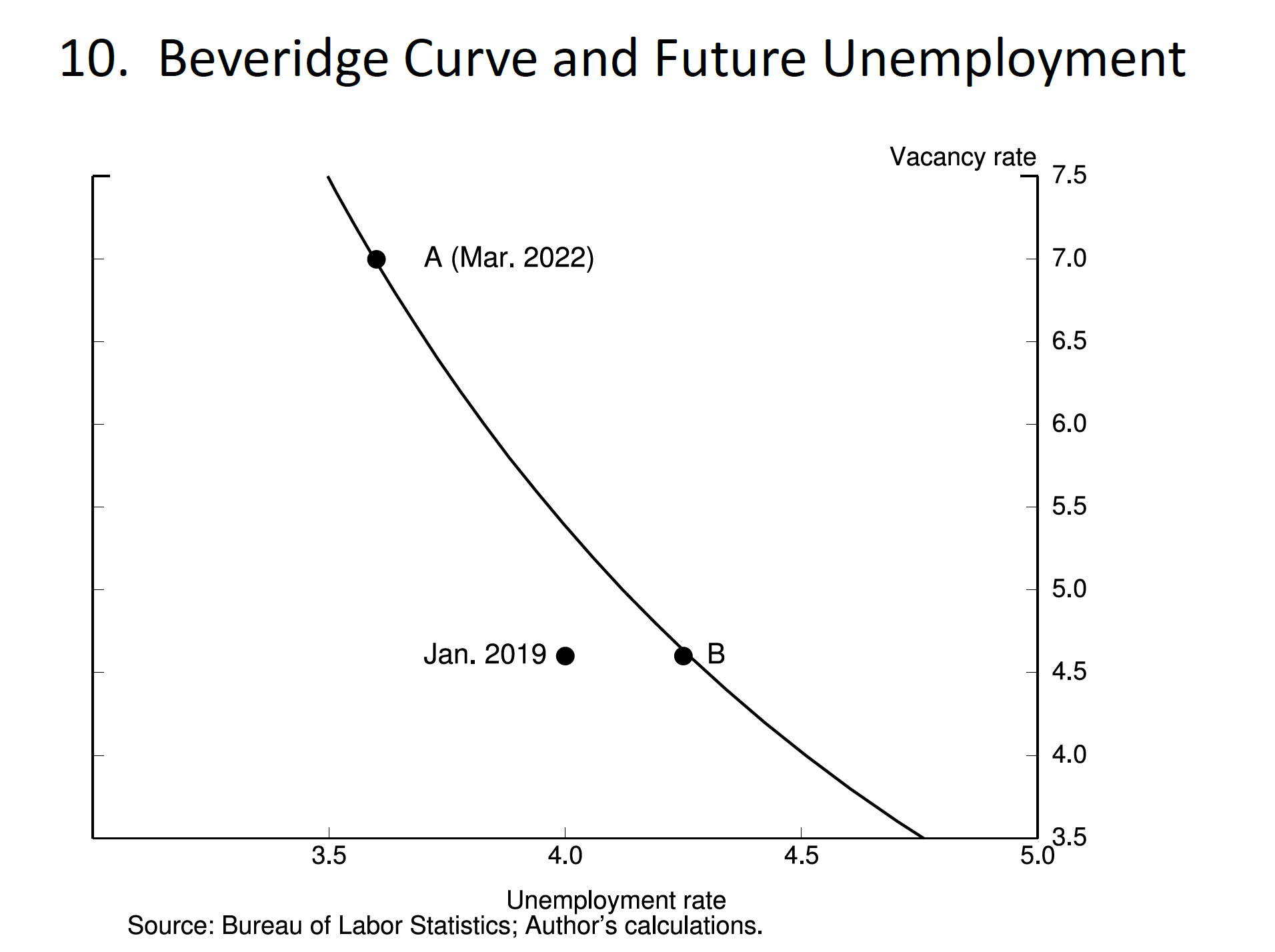

What does all this suggest about what will happen to the labor market when, as I expect, a tightening of financial conditions and fading fiscal stimulus start to cool labor demand? Slide 10 focuses on the Beveridge curve (the relationship produced by the direct effect of changes in vacancies on unemployment) when the separations rate is low, as it is now.7 The March 2022 observation lies at the top of the curve and is labeled point A. If there is cooling in aggregate demand spurred by monetary policy tightening that tempers labor demand, then vacancies should fall substantially. Suppose they decrease from the current level of 7 percent to 4.6 percent, the rate prevailing in January 2019, when the labor market was still quite strong. Then we should travel down the curve from point A to point B.8 The unemployment rate will increase, but only somewhat because labor demand is still strong — just not as strong — and because when the labor market is very tight, as it is now, vacancies generate relatively few hires. Indeed, hires per vacancy are currently at historically low levels. Thus, reducing vacancies from an extremely high level to a lower (but still strong) level has a relatively limited effect on hiring and on unemployment.

{kind=link}

Now, I also show the January 2019 observation of vacancies and unemployment. Recall, this is also where the economy was over the year prior to the pandemic. As you can see, moving from the March 2022 observation to the January 2019 observation is not that different from the change in the unemployment rate predicted by my estimated Beveridge curve, which suggests the predicted small increase in unemployment is a plausible outcome to policy tightening.

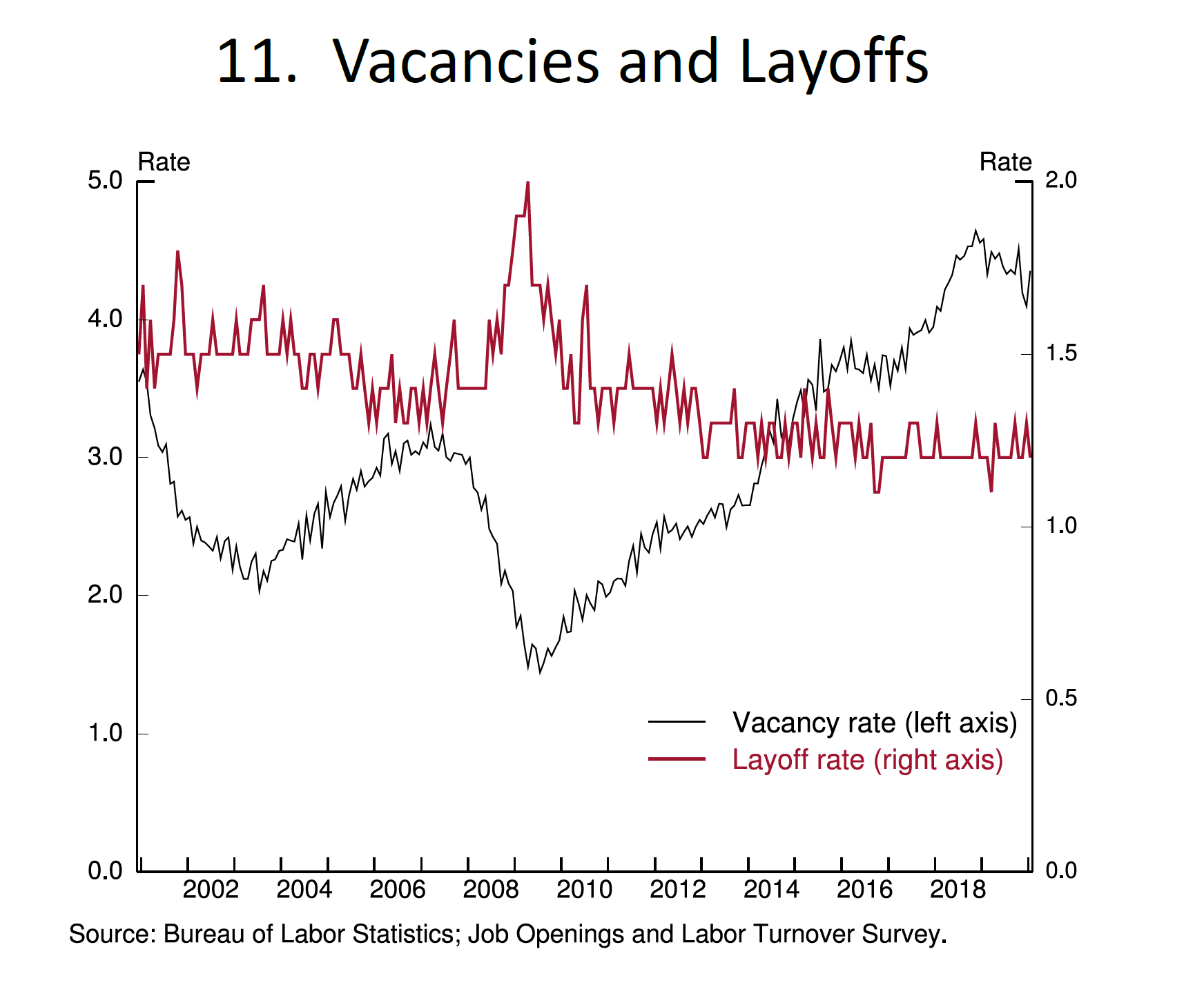

If labor demand cools, will separations increase and shift the curve outward, increasing unemployment further? I don't think so. As shown on slide 11, outside of recessions, layoffs don't change much. Instead, changes in labor demand appear to be reflected primarily in changes in vacancies.

{kind=link}

Now, it's certainly possible, even probable, that influences on the unemployment rate other than vacancies will change going forward. In terms of the equations we have been discussing, layoffs could increase somewhat, instead of staying constant. Matching efficiency could also improve or deteriorate. The vacancy rate could also change more or less than I have assumed. Thus, I'm not arguing that the unemployment rate will end up exactly as the Beveridge curve I've drawn suggests. But I do think it quite plausible that the unemployment rate will end up in the vicinity of what the Beveridge curve currently predicts.

Another consideration is that non-linear dynamics could take hold if the unemployment rate increases by a certain amount, as suggested by the Sahm rule, which holds that recessions have in the past occurred whenever the three-month moving average of the unemployment rate rises 0.5 percentage point over its minimum rate over the previous 12 months.9 We certainly need to be alert to this possibility, but the past is not always prescriptive of the future. The current situation is unique. We've never seen a vacancy rate of 7 percent before. Reducing the vacancy rate by 2.5 percentage points would still leave it at a level seen at the end of the last expansion, whereas in previous expansions a reduction of 2.5 percent would have left vacancies at or below 2 percent, a level only seen in extremely weak labor markets.

To sum up, the relationship between vacancies and unemployment gives me reason to hope that policy tightening in current circumstances can tame inflation without causing a sharp increase in unemployment. Of course, the path of the economy depends on many factors, including how the Ukraine war and COVID-19 evolve. From this discussion, I am left optimistic that the strong labor market can handle higher rates without a significant increase in unemployment.

In closing, I want to again thank the institute for the invitation to address you today, at a time of considerable challenge for Germany and the United States. It's not the first time we have faced such moments together. Just south of the Frankfurt Airport is a surprising sight — a couple of antique military cargo planes, parked on the side of the Autobahn. They were built by Douglas Aircraft, nearly 80 years ago, and stand today as monuments to one of the greatest achievements of cooperation between the freedom-loving people of Europe and those of the United States.

For 11 months, these two planes, and many others, took off and landed in perpetual motion, delivering 2.3 million tons of food, fuel, and other essentials to the people of Berlin, who were surrounded and besieged by Soviet forces. The commitment and ultimate triumph of this improbable airlift was in many ways the beginning of an alliance that has included ongoing economic cooperation that has strengthened both our democracies. In that spirit, I am certain we can both overcome the economic challenges that lie ahead.

More Articles

- Federal Reserve: Financial Stability in Uncertain Times, A Speech by Governor Michelle W. Bowman

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- Gender and Labor Markets by Diego Mendez-Carbajo* : "Sure [Fred Astaire] was great, but don't forget that Ginger Rogers did everything he did…backwards and in high heels." — Robert Thaves1

- The Federal Open Market Committee Statement: The Path of the Economy Continues to Depend On The Course Of The Virus

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Coronavirus Aid, Relief, and Economic Security Act; Chair Jerome H. Powell Before the Committee on Financial Services, House of Representatives

- Chair Jerome H. Powell: A Current Assessment of the Response to the Economic Fallout of this Historic Event

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- Federal Reserve Chair Jerome Powell Addresses Current Economic Issues: For Some, a Reversal of Economic Fortune