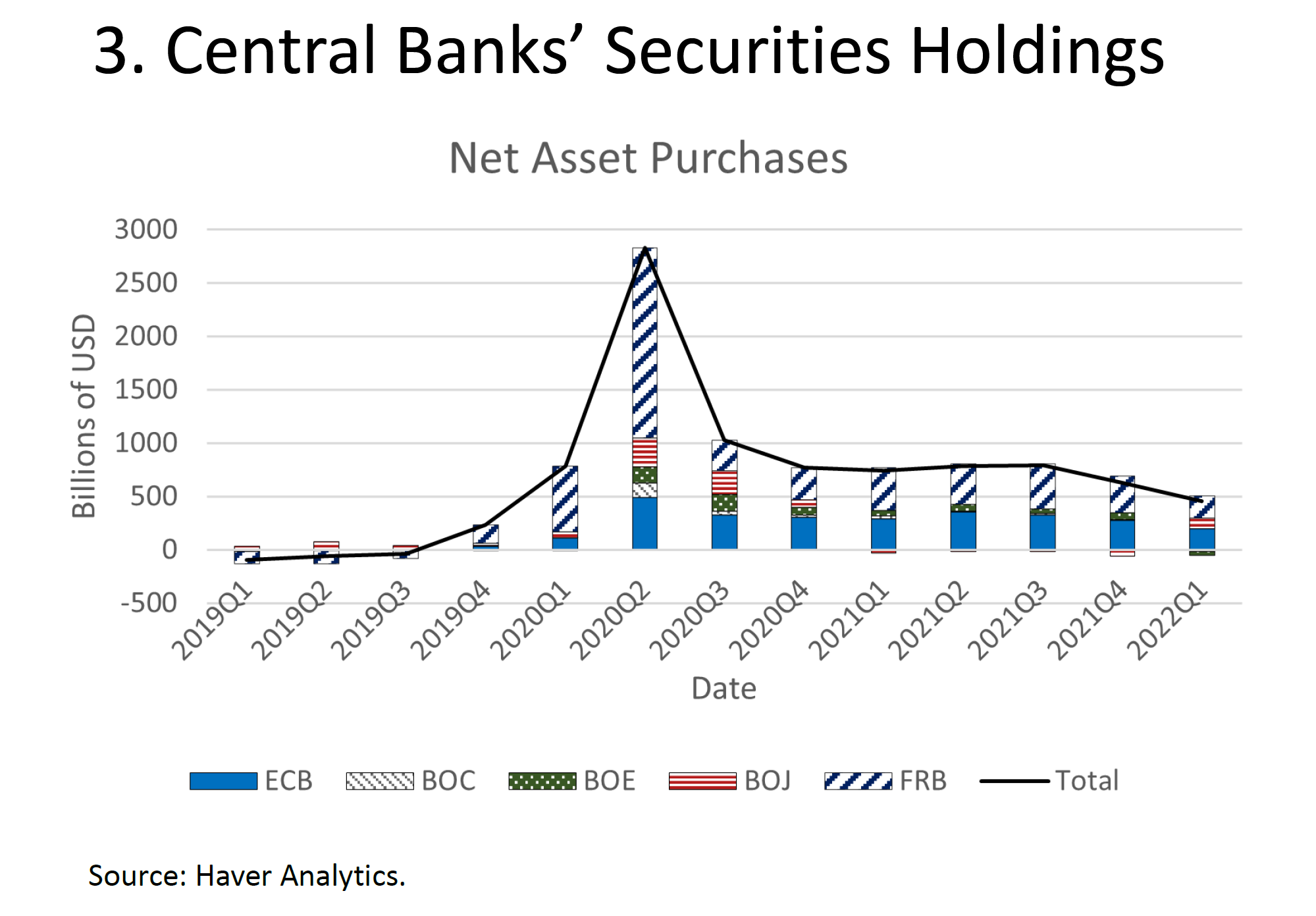

In addition to raising rates, the FOMC further tightened monetary policy by ending asset purchases in March and then agreeing to start reducing our holdings of securities, a process that begins June 1. By allowing securities to mature without reinvesting them, the Fed's balance sheet will shrink. We will phase in the amount of redemptions over three months. By September, we anticipate having up to $95 billion of securities rolling off the Fed's portfolio each month. This pace will reduce the Fed's securities holdings by about $1 trillion over the next year, and the reductions will continue until securities holdings are deemed close to the ample levels needed to implement policy efficiently and effectively. Although estimates are highly uncertain, using a variety of models and assumptions, the overall reduction in the balance sheet is estimated to be equivalent to a couple of 25-basis-point rate hikes.

All these actions have the goal of bringing inflation down toward the FOMC's 2 percent target. Increased rates and a smaller balance sheet raise the cost of borrowing and thus reduce household and business demand. On top of this, I also hope that over time supply problems resolve and help lower inflation. But the Fed isn't waiting for these supply constraints to resolve. We have the tools and the will to make substantial progress toward our target.

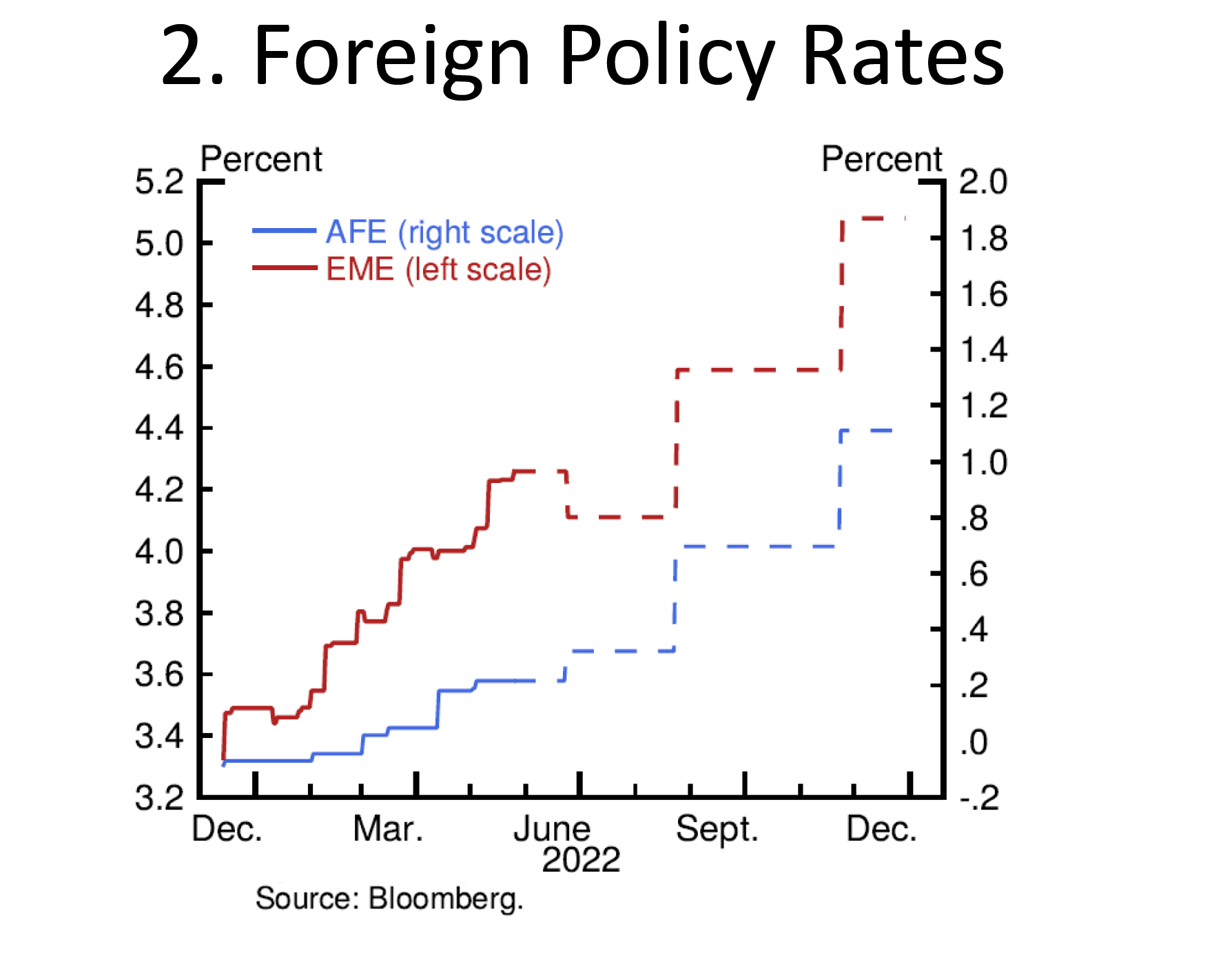

The United States is not alone in facing excessive inflation, and other central banks also are responding. There is a global shift toward monetary tightening. In the euro area, headline inflation continued to edge up in April, to 7.5 percent, while its version of core inflation increased from 2.9 percent to 3.5 percent. Based on this broadening of price pressures, communication by the European Central Bank (ECB) is widely interpreted as signaling that it will likely start raising its policy rate this summer and that it could raise rates a few times before year-end. Policy tightening started last year, as emerging markets including Mexico and Brazil increased rates substantially amid expectations of accelerating inflation. Several advanced-economy central banks, including the Bank of England, began raising interest rates in the second half of last year. Like the Fed, the Bank of Canada lifted off in March and, also like the Fed, picked up the pace of tightening with a rate hike of 50 basis points at its most recent meeting. Central banks in Australia and Sweden pivoted sharply to hike rates at their most recent meetings after previously saying that such moves were not likely anytime soon.

Slide 2 shows the similarly timed policy responses across advanced and emerging economy central banks in terms of actual and anticipated increases in their policy rates. Emerging market economies started the year with a policy rate that averaged around 3.5 percent, and they are expected to end the year averaging a bit over 5 percent. Advanced foreign economies started a bit below zero and at this point are expected to move up, on average, by around 1 percentage point. This worldwide increase in policy rates, unfortunately, reflects the fact that high inflation is a global problem, which central banks around the world recognize must be addressed.

{kind=link}

Finally, like the Fed, many other advanced-economy central banks that expanded their balance sheets over the past two years are now reversing course. In recent months, as shown in slide 3, the Bank of Canada and Bank of England have begun to shrink their balance sheets by stopping full reinvestment of maturing assets, similar to what the Fed will commence in June. Although the ECB has committed to reinvesting maturing assets for quite some time, it has tapered net purchases substantially since last year and has indicated it will likely end those purchases early in the third quarter.

{kind=link}

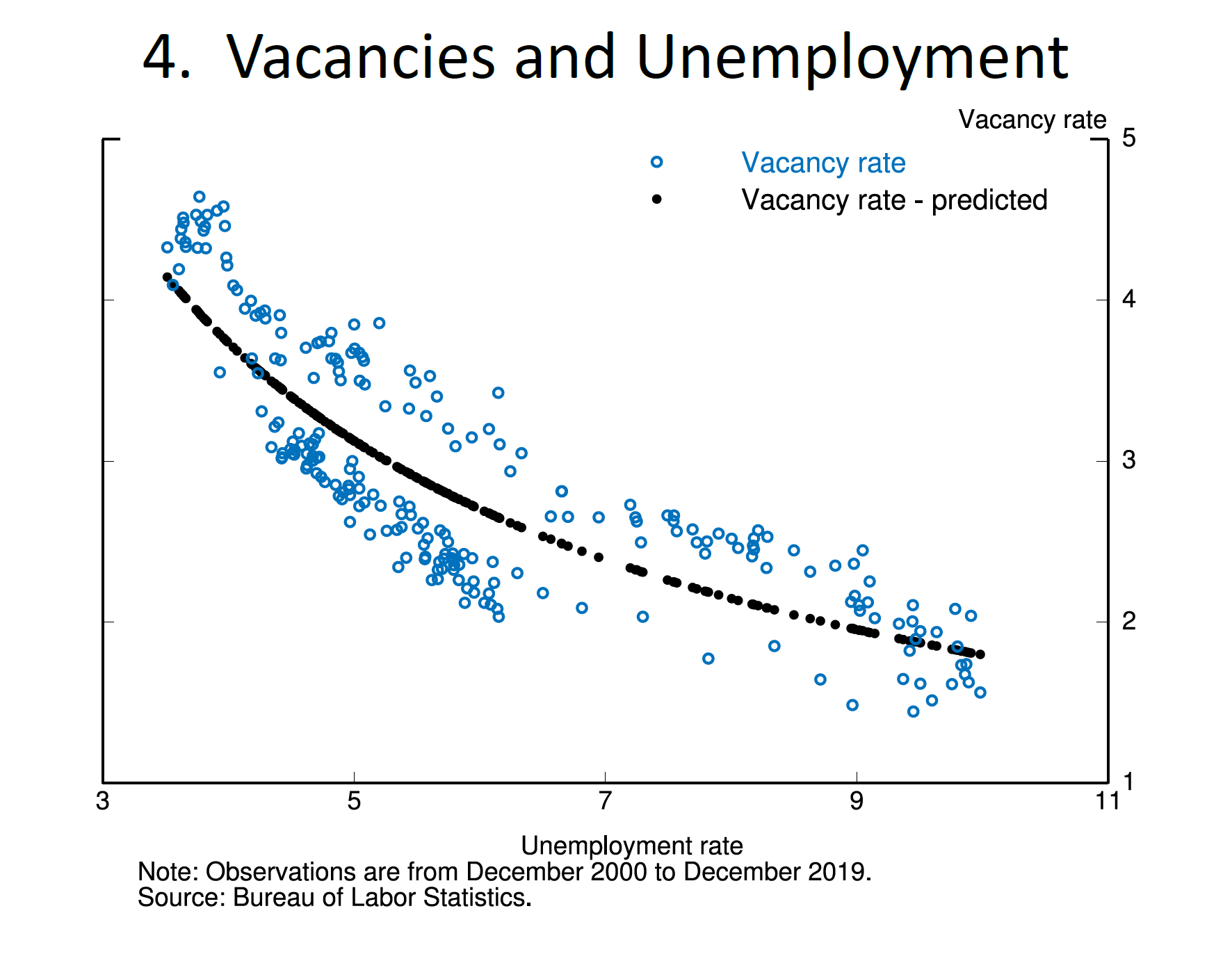

Some have expressed concern that the Fed cannot raise interest rates to arrest inflation while also avoiding a sharp slowdown in economic growth and significant damage to the labor market. One argument in this regard warns that policy tightening will reduce the current high level of job vacancies and push up unemployment substantially, based on the historical relationship between these two pieces of data, which is depicted by something called the Beveridge curve. Because I am now among fellow students of economics, I wanted to take a moment to show why this statement may not be correct in current circumstances.

First, a little background. The relationship between vacancies and the unemployment rate is shown in slide 4. The blue dots in the figure show observations of the vacancy rate and the unemployment rate between 2000 and 2018. The black curve is the fitted relationship between the log of vacancies and the log of unemployment over this period. It has a somewhat flat, downward slope. From this, the argument goes, policy to slow demand and push down vacancies requires moving along this curve and increasing the unemployment rate substantially.

{kind=link}

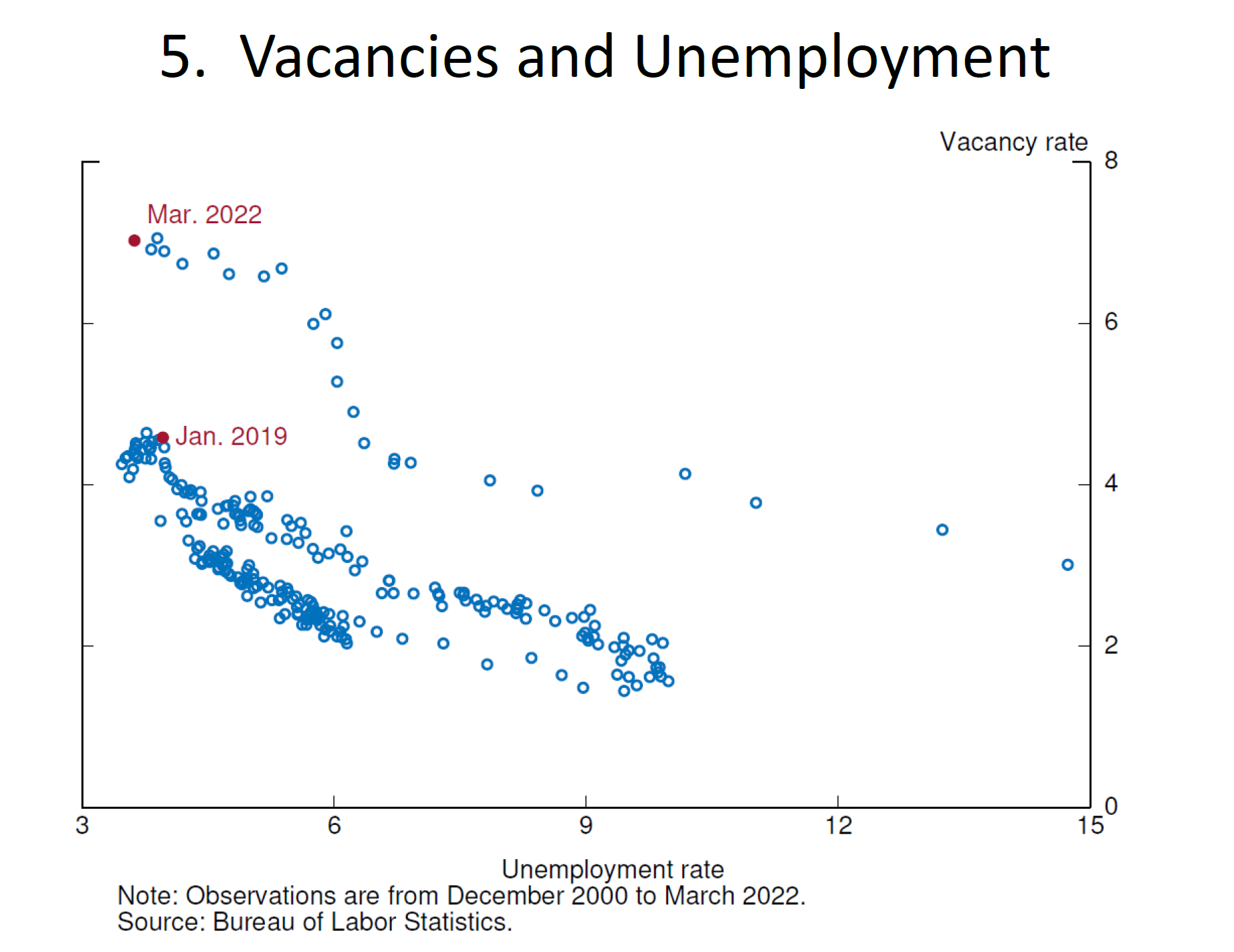

But there's another perspective about what a reduction in vacancies implies for unemployment that is just as plausible, if not more so. Slide 5 shows the same observations as slide 4 but also adds observations from the pandemic. The two larger red dots show the most recent observation, March 2022, and January 2019, when the vacancy rate had achieved its highest rate before the pandemic. These two dots suggest that the vacancy rate can be reduced substantially, from the current level to the January 2019 level, while still leaving the level of vacancies consistent with a strong labor market and with a low level of unemployment, such as we had in 2019. To see why this is a plausible outcome, I first need to digress a bit to discuss the important determinants of unemployment.

{kind=link}

More Articles

- Federal Reserve: Financial Stability in Uncertain Times, A Speech by Governor Michelle W. Bowman

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- Gender and Labor Markets by Diego Mendez-Carbajo* : "Sure [Fred Astaire] was great, but don't forget that Ginger Rogers did everything he did…backwards and in high heels." — Robert Thaves1

- The Federal Open Market Committee Statement: The Path of the Economy Continues to Depend On The Course Of The Virus

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Coronavirus Aid, Relief, and Economic Security Act; Chair Jerome H. Powell Before the Committee on Financial Services, House of Representatives

- Chair Jerome H. Powell: A Current Assessment of the Response to the Economic Fallout of this Historic Event

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- Federal Reserve Chair Jerome Powell Addresses Current Economic Issues: For Some, a Reversal of Economic Fortune