Let me turn now to the outlook for the Fed's top priority, inflation. I said in December that inflation was alarmingly high, and it has remained so. The April consumer price index (CPI) was up 8.3 percent year over year. This headline number was a slight decline from 8.5 percent in March but primarily due to a drop in volatile gasoline prices that we know surged again this month. Twelve-month "core" inflation, which strips out volatile food and energy prices, was also down slightly to 6.2 percent in April, from 6.5 percent the month before, but the 0.6 percent monthly increase from March was an acceleration from the February to March rate and still too high. Meanwhile, the Fed's preferred measure based on personal consumption expenditures (PCE) recorded headline inflation of 6.3 percent and core of 4.9 percent. These lower readings relative to CPI reflect differences in the weights of various categories across these indexes. No matter which measure is considered, however, headline inflation has come in above 4 percent for about a year and core inflation is not coming down enough to meet the Fed's target anytime soon. Inflation this high affects everyone but is especially painful for lower- and middle-income households that spend a large share of their income on shelter, groceries, gasoline, and other necessities. It is the FOMC's job to meet our price stability mandate and get inflation down, and we are determined to do so.

The forces driving inflation today are the same ones that emerged a year ago. The combination of strong consumer demand and supply constraints—both bottlenecks and a shortage of workers relative to labor demand—is generating very high inflation. We can argue about whether supply or demand is a greater factor, but the details have no bearing on the fact that we are not meeting the FOMC's price stability mandate. What I care about is getting inflation down so that we avoid a lasting escalation in the public's expectations of future inflation. Once inflation expectations become unanchored in this way, it is very difficult and economically painful to lower them.

While it is not surprising that inflation expectations for the next year are up, since current inflation is high, what I focus on is longer-term inflation expectations. Recent data that try to measure longer-term expectations are mixed. Overall, my assessment is that longer-range inflation expectations have moved up from a level that was consistent with trend inflation below 2 percent to a level that's consistent with underlying inflation a little above 2 percent. I will be watching that these expectations do not continue to rise because longer-term inflation expectations influence near term inflation, as well as our ability to achieve our 2 percent target. When they are anchored, they influence spending decisions today in a way that helps inflation move toward our target. To ensure these longer-term expectations do not move up broadly, the Federal Reserve has tools to reduce demand, which should ease inflation pressures. And, over time, supply constraints will resolve to help rein in price increases as well, although we don't know how soon.

I cannot emphasize enough that my FOMC colleagues and I are united in our commitment to do what it takes to bring inflation down and achieve the Fed's 2 percent target. Since the start of this year, the FOMC has raised the target range for the federal funds rate by 75 basis points, with 50 basis points of that increase coming at our meeting earlier this month. We also issued forward guidance about the likely path of policy. The May FOMC statement said the Committee "anticipates that ongoing increases in the target range will be appropriate."

I support tightening policy by another 50 basis points for several meetings. In particular, I am not taking 50 basis-point hikes off the table until I see inflation coming down closer to our 2 percent target. And, by the end of this year, I support having the policy rate at a level above neutral so that it is reducing demand for products and labor, bringing it more in line with supply and thus helping rein in inflation. This is my projection today, given where we stand and how I expect the economy to evolve. Of course, my future decisions will depend on incoming data. In the next couple of weeks, for example, the May employment and CPI reports will be released. Those are two key pieces of data I will be watching to get information about the continuing strength of the labor market and about the momentum in price increases. Over a longer period, we will learn more about how monetary policy is affecting demand and how supply constraints are evolving. If the data suggest that inflation is stubbornly high, I am prepared to do more.

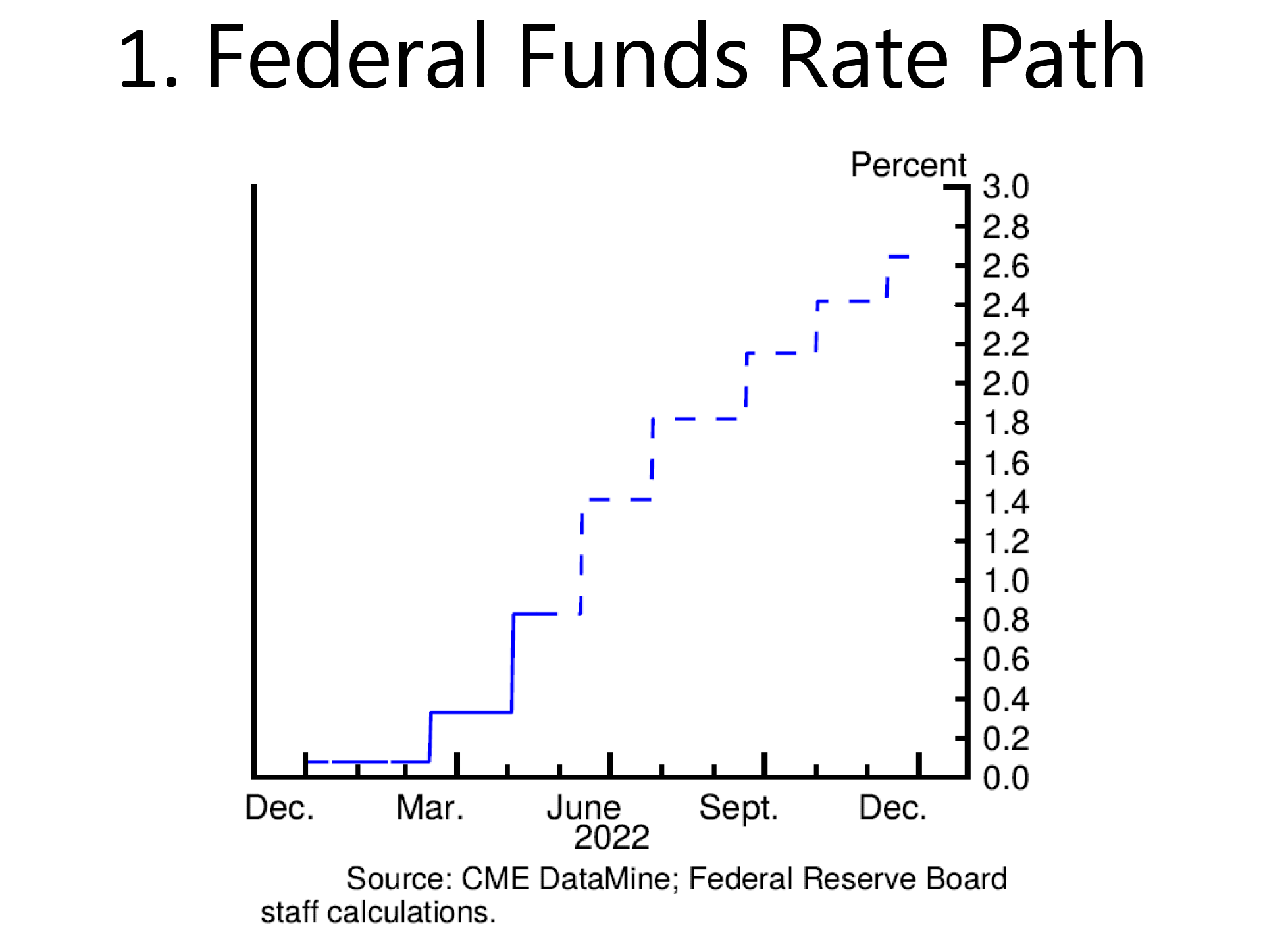

My plan for rate hikes is roughly in line with the expectations of financial markets. As seen in slide 1, federal funds futures are pricing in roughly 50 basis point hikes at the FOMC's next two meetings and expecting the year-end policy rate to be around 2.65 percent. So, in total, markets expect about 2.5 percentage points of tightening this year. This expectation represents a significant degree of policy tightening, consistent with the FOMC's commitment to get inflation back under control and, if we need to do more, we will.

{kind=link}

These current and anticipated policy actions have already resulted in a significant tightening of financial conditions. The benchmark 10-year Treasury security began the year at a yield of around 1.5 percent and has risen to around 2.8 percent. Rates for home mortgages are up 200 basis points, and other credit financing costs have followed suit. Higher rates make it more expensive to finance spending and investment which should help reduce demand and contribute to lower inflation.

More Articles

- Federal Reserve: Financial Stability in Uncertain Times, A Speech by Governor Michelle W. Bowman

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- Gender and Labor Markets by Diego Mendez-Carbajo* : "Sure [Fred Astaire] was great, but don't forget that Ginger Rogers did everything he did…backwards and in high heels." — Robert Thaves1

- The Federal Open Market Committee Statement: The Path of the Economy Continues to Depend On The Course Of The Virus

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Coronavirus Aid, Relief, and Economic Security Act; Chair Jerome H. Powell Before the Committee on Financial Services, House of Representatives

- Chair Jerome H. Powell: A Current Assessment of the Response to the Economic Fallout of this Historic Event

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- Federal Reserve Chair Jerome Powell Addresses Current Economic Issues: For Some, a Reversal of Economic Fortune