Core inflation—inflation excluding volatile food and energy prices—also moderated in July. Core goods PCE inflation decelerated to 0.1 percent month-over-month in July after averaging 0.5 percent in May and June.6 While the moderation in monthly inflation is welcome, it will be necessary to see several months of low monthly inflation readings to be confident that inflation is moving back down to 2 percent.

How long it takes to move inflation back down to 2 percent will depend on a combination of continued easing in supply constraints, slower demand growth, and lower markups, against the backdrop of anchored expectations. With regard to supply constraints, a variety of indicators are showing signs of improvement on delivery times and supplies of some goods. In addition, labor force participation showed a welcome increase in the August employment data, particularly in the boost in participation among women in the core working years of 25 to 54 years of age. Even with this improvement, the participation rate is still 1 percentage point below its pre-pandemic level, well in excess of the decline in the participation rate that would have been expected due to retirements in the absence of the pandemic.

Reductions in markups could also make an important contribution to reduced pricing pressures. Last year's rapid demand growth in the face of supply constraints led to product shortages in some areas of the economy and high margins for many firms. Although we are hearing some reports of large retailers planning markdowns due to excess inventories, we do not have hard data at an aggregate level suggesting that businesses are reducing margins in response to more price sensitivity among customers. At an aggregate level, in the second quarter, measures of profits in the nonfinancial sector relative to GDP remained near the postwar peak reached last year.7

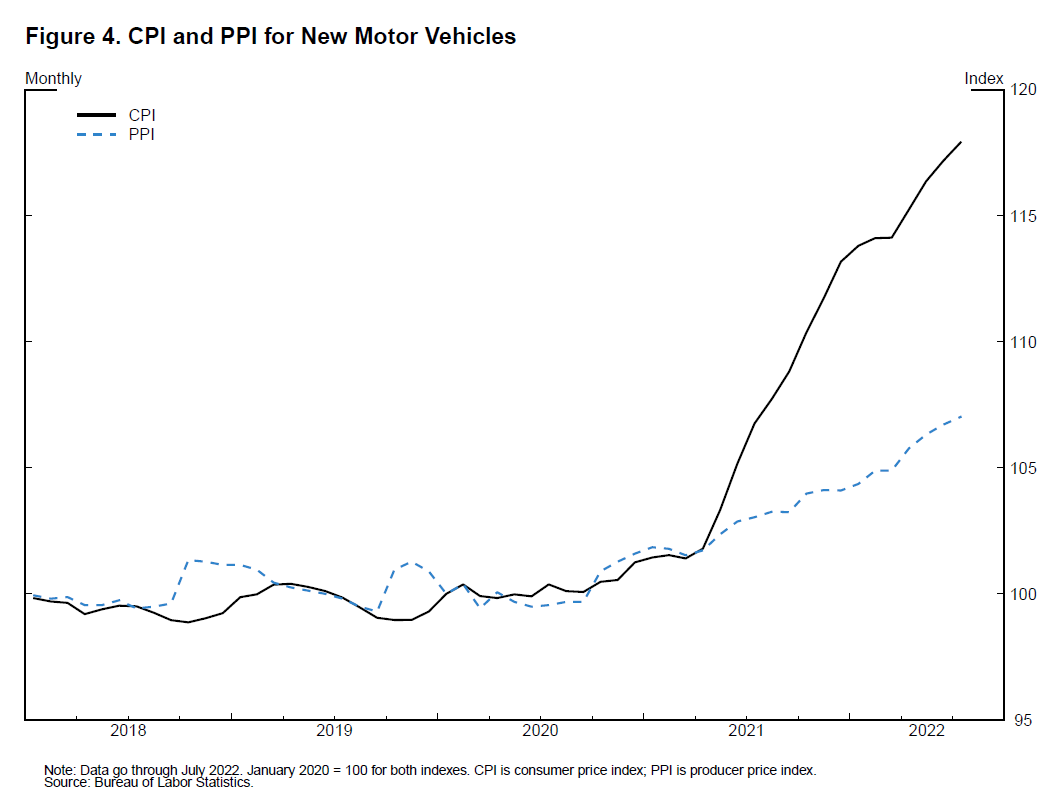

Using the available macroeconomic data, it is challenging to measure directly how much firms mark up their prices relative to their costs. That said, there is evidence at the sectoral level that margins remain high in areas such as motor vehicles and retail. After moving together closely for several years, starting early last year, the new motor vehicle consumer price index (CPI), which measures the price dealers charge to customers, diverged from the equivalent producer price index (PPI), which measures the price dealers paid to manufacturers. Since then, the CPI has increased three times faster than the PPI (figure 4). This divergence between retail and wholesale prices suggests an unusually large retail auto margin. With production now increasing, and interest-sensitive demand cooling, there may soon be pressures to reduce vehicle margins and prices in order to move the higher volume of cars being produced off dealer lots.

{kind=link}

Similarly, overall retail margins—the difference between the price retailers charge for a good and the price retailers paid for that good—have risen significantly more than the average hourly wage that retailers pay workers to stock shelves and serve customers over the past year, suggesting that there may also be scope for reductions in retail margins. With gross retail margins amounting to about 30 percent of sales, a reduction in currently elevated margins could make an important contribution to reduced inflation pressures in consumer goods.

Labor demand continues to exhibit considerable strength, which is hard to reconcile with the more downbeat tone of activity. Year-to-date through August, payroll employment has increased by about 3-1/2 million jobs, a surprisingly strong increase given the decelerating spending and declining GDP over the first half of the year. The unemployment rate has fallen, on net, from 4 percent in January to 3.7 percent in August. Possibly the strongest indications that the labor market is tight were the first- and second-quarter readings of the employment cost index (ECI), which point to strong and broad-based growth in total hourly compensation. The 6.3 percent reading for the ECI in the second quarter was the largest annualized quarterly growth in compensation under this metric since 1982. The most recent reading of average hourly earnings suggested some possible cooling, decelerating from a gain of 0.5 percent in July to 0.3 percent in August, although it will be important to see additional data.

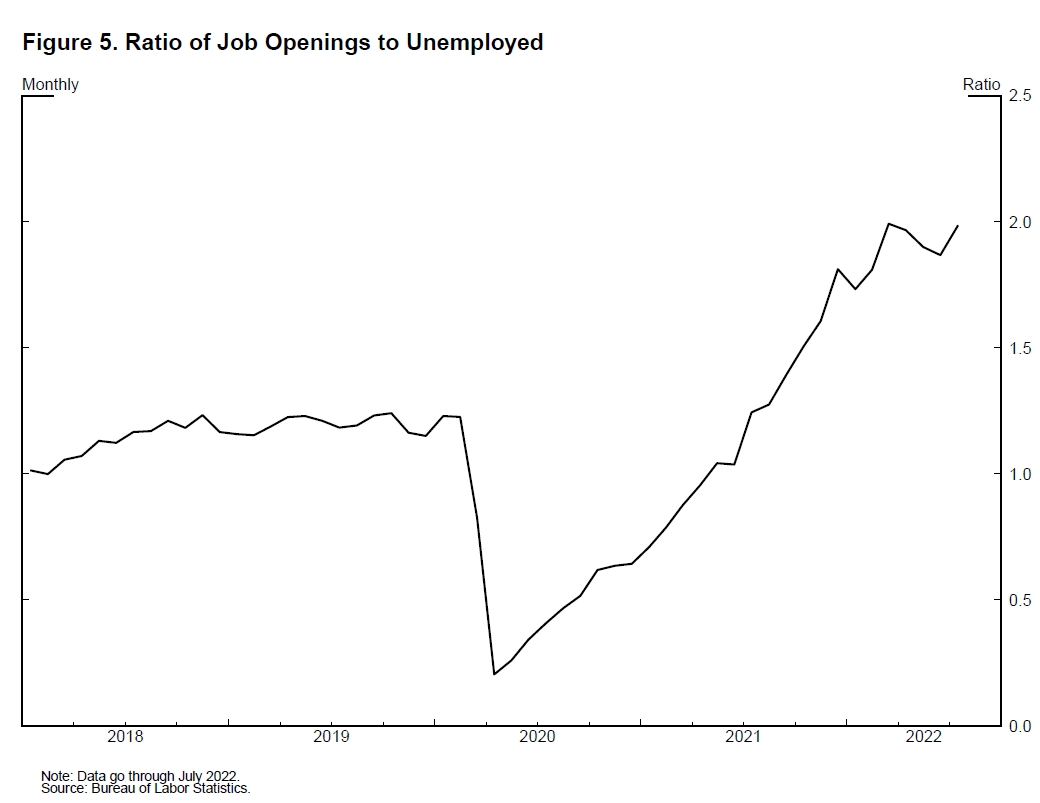

The deceleration in economic activity thus far this year has coincided with only a slight easing in job openings, on net, since their peak in March. The current high level of job openings relative to job seekers remains close to the largest in postwar history, consistent with a tight labor market (figure 5). Businesses that experienced unprecedented challenges restoring or expanding their workforces following the pandemic may be more inclined to make greater efforts to retain their employees than they normally would when facing a slowdown in economic activity. This may mean that slowing aggregate demand will lead to a smaller increase in unemployment than we have seen in previous recessions, but it is too early to draw any definitive conclusions, and I will be monitoring a variety of labor market indicators closely.8

{kind=link}