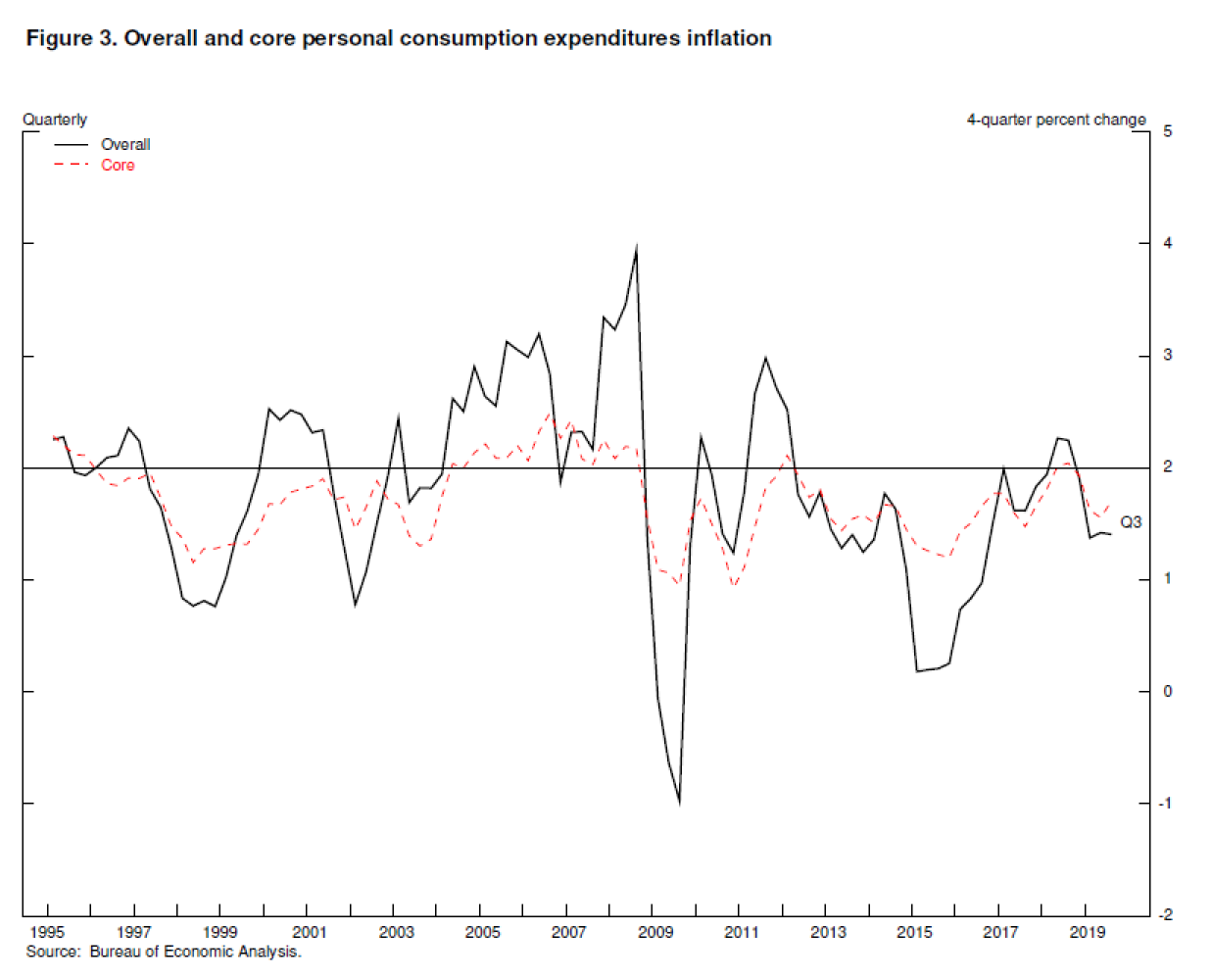

A Sustained Return of Inflation to 2 percent

For many years as the economy recovered from the Great Recession, inflation averaged around 1.5 percent—below our 2 percent objective (figure 3). We had long expected that inflation would gradually rise as the expansion continued, and, as I noted, both overall and core inflation ran at rates consistent with our goal for much of 2018. But this year, inflation is again running below 2 percent.

{kind=link}

It is reasonable to ask why inflation running somewhat below 2 percent is a big deal. We have heard a lot about inflation at our Fed Listens events. People are concerned about the rising cost of medical care, of housing, and of college, but nobody seems to be complaining about overall inflation running below 2 percent. Even central bankers are not concerned about any particular minor fluctuation in inflation.

Around the world, however, we have seen that inflation running persistently below target can lead to an unhealthy dynamic in which inflation expectations drift down, pulling actual inflation further down. Lower inflation can, in turn, pull interest rates to ever-lower levels. The experience of Japan, and now the euro area, suggests that this dynamic is very difficult to reverse, and once under way, it can make it harder for a central bank to support its economy by further lowering interest rates. That is why it is essential that we at the Fed use our tools to make sure that we do not permit an unhealthy downward drift in inflation expectations and inflation. We are strongly committed to symmetrically and sustainably achieving our 2 percent inflation objective so that in making long-term plans, households and businesses can reasonably expect 2 percent inflation over time.

Spreading the Benefits of Employment

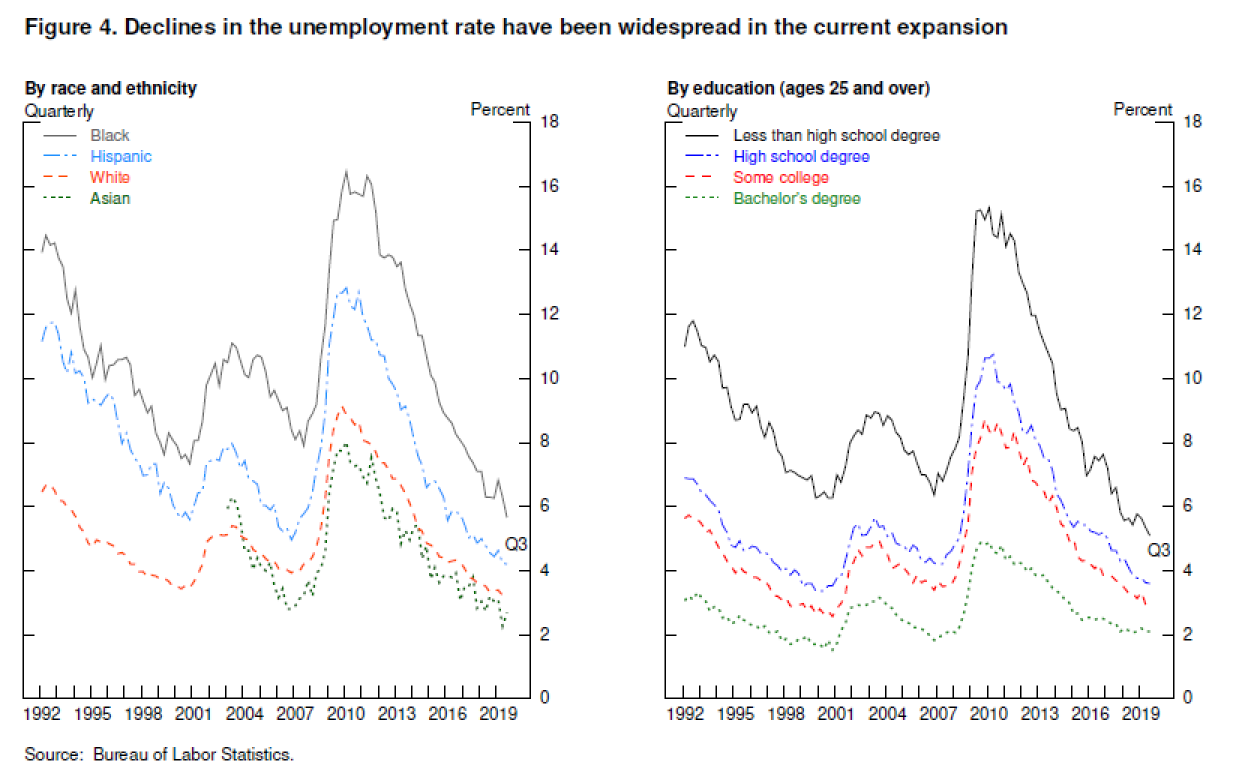

Many people at our Fed Listens events have told us that this long expansion is now benefiting low- and middle-income communities to a degree that has not been felt for many years. We have heard about companies, communities, and schools working together to help employees build skills—and of employers working creatively to structure jobs so that employees can do their jobs while coping with the demands of family and life beyond the workplace. We have heard that many people who in the past struggled to stay in the workforce are now working and adding new and better chapters to their lives. These stories show clearly in the job market data. Employment gains have been broad based across all racial and ethnic groups and all levels of educational attainment as well as among people with disabilities (figure 4).

{kind=link}

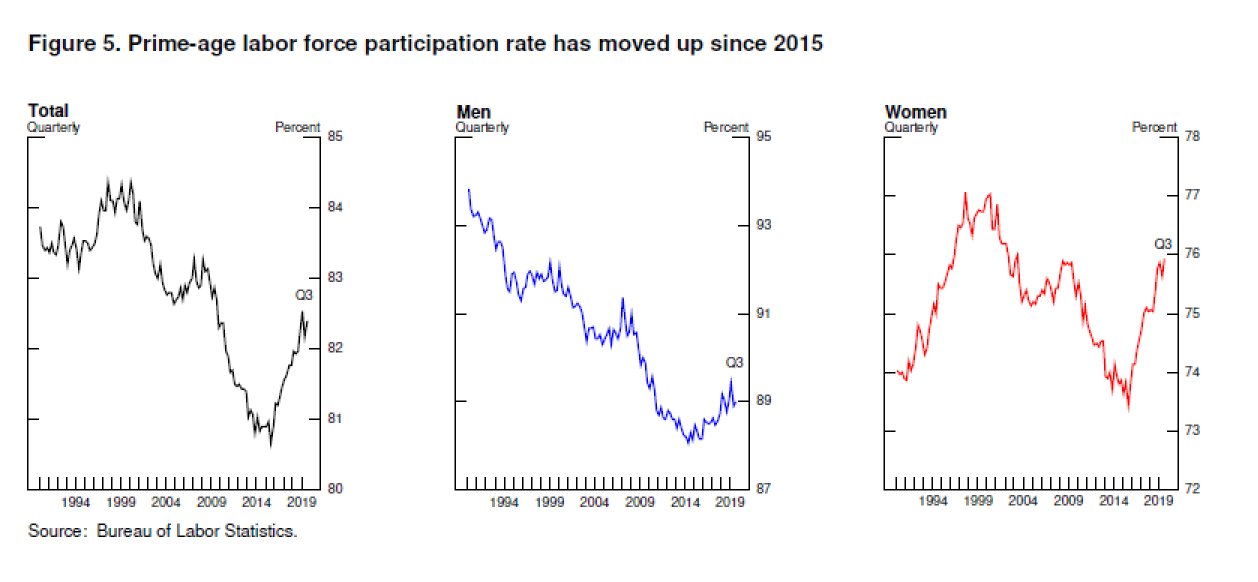

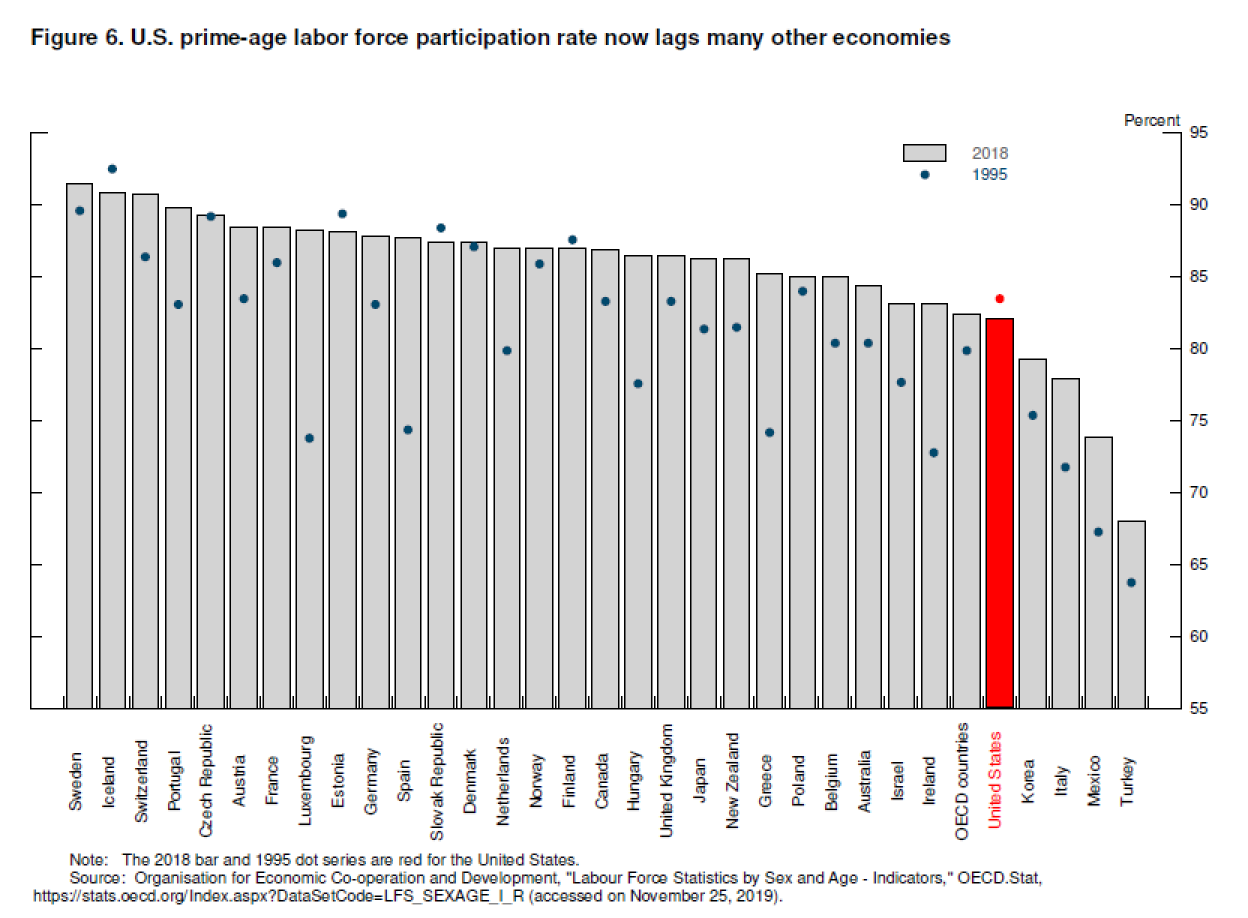

The strong labor market is also encouraging more people in their prime working years—ages 25 to 54—to rejoin or remain in the labor force, meaning that they either have a job or are actively looking for one. This is a welcome development. For several decades up until the mid-1990s, the share of prime-age people in the labor force rose, as an influx of women more than offset some decline in male participation. In the mid-1990s, however, prime-age participation began to fall, and the drop-off became steeper in the Great Recession and the early years of the recovery (figure 5). Between 2007 and 2013, falling participation by both men and women contributed to a 2 percentage point overall decline. Our falling participation rate stands out among advanced economies. While the United States was roughly in the middle of the pack among 32 economies as of 1995, in 2018 we ranked near the bottom (figure 6). Fortunately, in the strong job market since 2014, prime-age participation has been staging a comeback. So far, we have made up more than half the loss in the Great Recession, which translates to almost 2 million more people in the labor force. But prime age participation could be still higher.

{kind=link}

{kind=link}

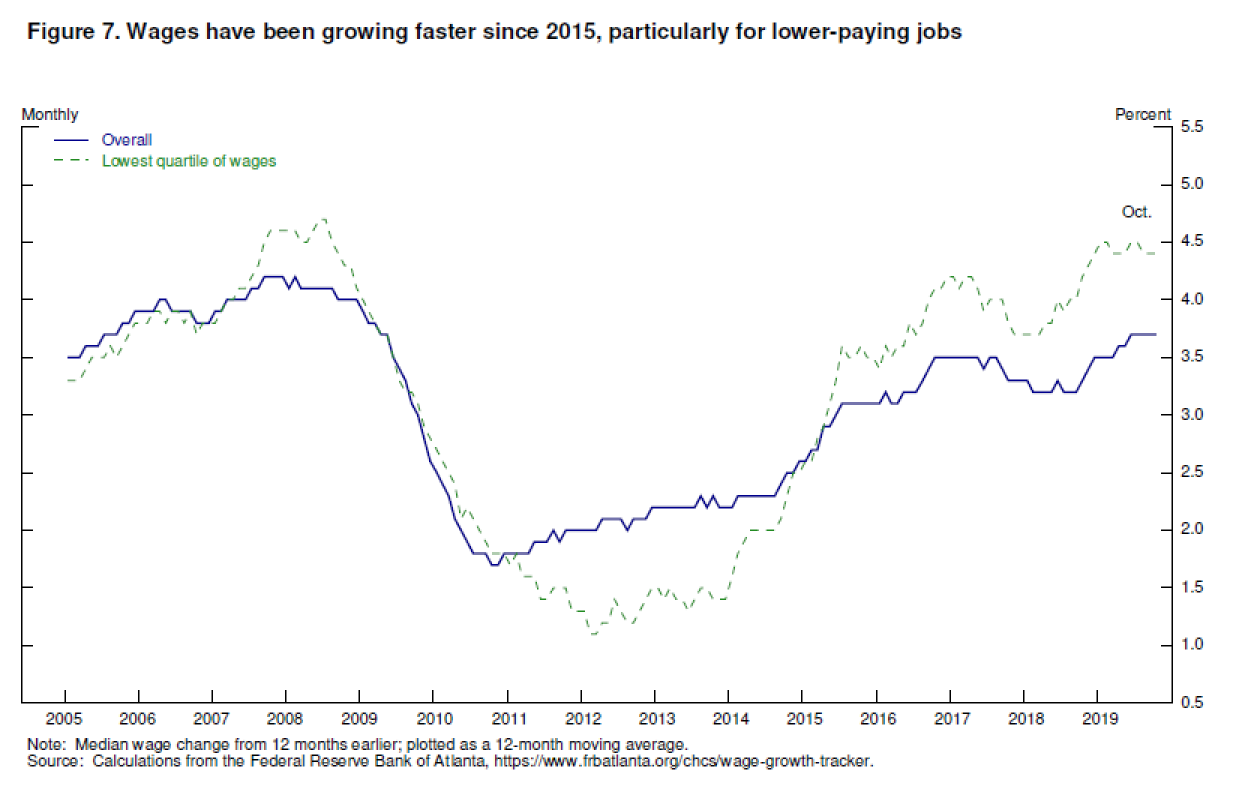

Income growth of low- and middle-income households has shown a pattern similar to that of participation, with two decades of disappointing news turning to better news during the past few years. According to Census data, inflation-adjusted incomes for the lowest 20 percent of households declined slightly over the two decades through 2014, and income for the middle 20 percent rose only modestly. Since then, incomes for these groups have risen more rapidly, as wage growth has picked up—and picked up most for the lower-paying jobs (figure 7).

{kind=link}

Recent years' data paint a hopeful picture of more people in their prime years in the workforce and wages rising for low- and middle-income workers. But as the people at our Fed Listens events emphasized, this is just a start: There is still plenty of room for building on these gains. The Fed can play a role in this effort by steadfastly pursuing our goals of maximum employment and price stability. The research literature suggests a variety of policies, beyond the scope of monetary policy, that could spur further progress by better preparing people to meet the challenges of technological innovation and global competition and by supporting and rewarding labor force participation.6 These policies could bring immense benefits both to the lives of workers and families directly affected and to the strength of the economy overall. Of course, the task of evaluating the costs and benefits of these policies falls to our elected representatives.

Conclusion

Monetary policy is now well positioned to support a strong labor market and return inflation decisively to our symmetric 2 percent objective. If the outlook changes materially, policy will change as well. At this point in the long expansion, I see the glass as much more than half full. With the right policies, we can fill it further, building on the gains so far and spreading the benefits more broadly to all Americans.

1. These wealth calculations are from the Federal Reserve's Distributional Financial Accounts (DFAs). For more details on the DFAs, see Michael Batty, Joseph Briggs, Karen Pence, Paul Smith, and Alice Volz (2019), "The Distributional Financial Accounts," FEDS Notes (Washington: Board of Governors of the Federal Reserve System, August 30). To view or download the data, see the interactive visualization tool at https://www.federalreserve.gov/releases/z1/dataviz/dfa/index.html. Return to text

2. The projections of FOMC participants as reported in the Summary of Economic Projections show a similar change. Return to text

3. The Fed's real-time assessment of job growth this year is discussed in Jerome H. Powell (2019), "Data-Dependent Monetary Policy in an Evolving Economy," speech delivered at "Trucks and Terabytes: Integrating the 'Old' and 'New' Economies," the 61st Annual Meeting of the National Association for Business Economics, Denver, Colorado, October 8. Return to text

4. Averaging across the estimates in figure 2, the estimates of r* are down 0.3 percentage point and those of u* are down 0.2 percentage point. Return to text

5. Taken literally, the revised estimates of the stars would, by standard rules of thumb, call for a somewhat lower federal funds rate. For example, using the Taylor (1993) rule and using Okun's law to state the rule in terms of the unemployment gap with a coefficient of 1 instead of the output gap with a coefficient of 0.5, the shift in r* and u* would call for a 50 basis point reduction in the federal funds rate. John B. Taylor (1993), "Discretion versus Policy Rules in Practice," Carnegie-Rochester Conference Series on Public Policy, vol. 39 (December) (New York: Elsevier), pp. 195–214. Return to text

6. Francesco Grigoli, Zsóka Kóczán, and Petia Topalova (2018), "Labor Force Participation in Advanced Economies: Drivers and Prospects (PDF)," chapter 2 in International Monetary Fund, World Economic Outlook (Washington: IMF, April), pp. 1–58. Return to text

More Articles

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022

- Reflections on Monetary Policy in 2021 By Federal Reserve Governor Christopher J. Waller or "How did the Fed get so far behind the curve?"

- Jerome Powell's Testimony at His Nomination Hearing for a Second Term as Chair of the Board of Governors of the Federal Reserve System; A Link to The Beige Book

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Prices are Spiking for Homes, Cars and Gas; Don’t Be Alarmed, Economists Say

- New Economic Challenges and the Fed's Monetary Policy Review by Chair of the Federal Reserve Jerome H. Powell