As the year began, growth appeared robust, but the economy faced some risks flowing mainly from weakening global economic growth and trade developments. Foreign growth, which slipped in the second half of last year, slid further as 2019 progressed. While weaker foreign growth does not necessarily translate into similar weakness here, it does hurt our exporters and presents a risk that the weakness may spread more broadly. At the same time, business contacts around the country have been telling us that trade-related uncertainties are weighing on their decisions. These global developments have been holding back overall economic growth. Manufacturing output, which had only recently surpassed its level before the Great Recession, has declined this year and is again below its pre-recession peak. Business investment has also weakened.

In addition, inflation pressures proved unexpectedly muted this year. After remaining close to our symmetric 2 percent objective for much of last year, inflation is now running below 2 percent. Some of the softness in overall inflation is the result of a fall in oil prices and should not affect inflation going forward. But core inflation—which omits volatile food and energy prices—is also running somewhat below 2 percent.

The main themes of our deliberations this year have been a continuing favorable outlook founded on strength in the household sector, with a few yellow flags including muted inflation and weakness in manufacturing. In addition, global growth and trade have presented ongoing risks and uncertainties. We also faced some less prominent factors that always confront policymakers. Specifically, we never have a crystal clear real-time picture of how the economy is performing. In addition, the precise timing and size of the effects of our policy decisions cannot be known in real time.

In August, the Bureau of Labor Statistics previewed a likely revision to its count of payroll job creation for the 12 months ended March 2019. The preview indicated that job gains over that period were about half a million lower than previously reported. On a monthly basis, job gains were likely about 170,000 per month, rather than 210,000. While this news did not dramatically alter our outlook, it pointed to an economy with somewhat less momentum than we had thought.3

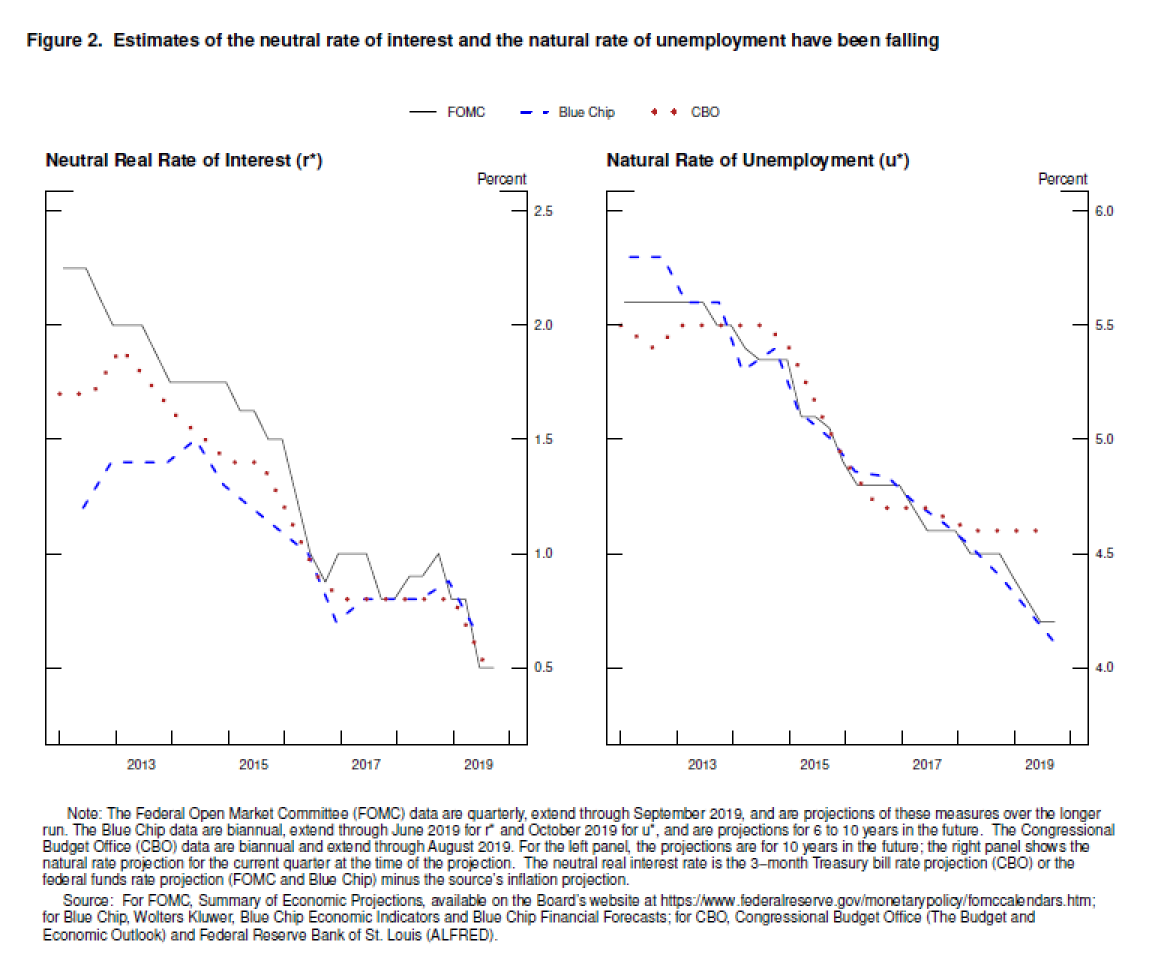

Uncertainty about how our policies are affecting the economy also entered our discussions. As you know, we set our policy interest rate to achieve our goals of maximum employment and stable prices. In doing so, we often refer to certain benchmarks. One of these is the interest rate that would be neutral — neither restraining the economy nor pushing it upward. We call that rate "r*" (pronounced "r star"). A policy rate above r* would tend to restrain economic activity, while a setting below r* would tend to speed up the economy. A second benchmark is the natural rate of unemployment, which is the lowest rate of unemployment that would not create upward pressure on inflation. We call that rate "u*" (pronounced "u star"). You can think of r* and u* as two of the main stars by which we navigate.

In an ideal world, policymakers could rely on these stars like mariners before the advent of GPS. But, unlike celestial stars on a clear night, we cannot directly observe these stars, and their values change in ways that are difficult to track in real time. Standard estimates of r* and u* made by policymakers and other analysts have been falling since 2012 (figure 2). Since the end of last year, incoming data — especially muted inflation data — prompted analysts inside and outside the Fed to again revise down their estimates of r* and u*.4 Taken at face value, a lower r* would suggest that monetary policy is providing somewhat less support for employment and inflation than previously believed, and the fall in u* would suggest that the labor market was less tight than believed.5 Both could help explain the weakness in inflation. As with the revised jobs data, these revised estimates of the stars were not a game changer for policy, but they provided another reason why a somewhat lower setting of our policy interest rate might be appropriate.

{kind=link}

How did we add up all of these considerations? To help keep the US economy strong in the face of global developments and to provide some insurance against ongoing risks, we progressively eased the stance of monetary policy over the course of the year. First, we signaled that increases in our short-term interest rate were unlikely. Then, from July to October, we reduced the target range for the federal funds rate by 3/4 percentage point. The full effects of these monetary policy actions will be felt over time, but we believe they are already helping to support consumer and business sentiment and boosting spending in interest-sensitive sectors, such as housing and consumer durable goods.

We see the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with our outlook of moderate economic growth, a strong labor market, and inflation near our symmetric 2 percent objective. Looking ahead, we will be monitoring the effects of our policy actions, along with other information bearing on the outlook, as we assess the appropriate path of the target range for the federal funds rate. Of course, if developments emerge that cause a material reassessment of our outlook, we would respond accordingly. Policy is not on a preset course.

I will wrap up with two areas where we have an opportunity to build on our gains.

More Articles

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022

- Reflections on Monetary Policy in 2021 By Federal Reserve Governor Christopher J. Waller or "How did the Fed get so far behind the curve?"

- Jerome Powell's Testimony at His Nomination Hearing for a Second Term as Chair of the Board of Governors of the Federal Reserve System; A Link to The Beige Book

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Prices are Spiking for Homes, Cars and Gas; Don’t Be Alarmed, Economists Say

- New Economic Challenges and the Fed's Monetary Policy Review by Chair of the Federal Reserve Jerome H. Powell