New Economic Challenges and the Fed's Monetary Policy Review by Chair of the Federal Reserve Jerome H. Powell

August 27, 2020

Chair Jerome H. Powell

At "Navigating the Decade Ahead: Implications for Monetary Policy," an economic policy symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming (via webcast)

Thank you, Esther, for that introduction, and good morning. The Kansas City Fed's Economic Policy Symposiums have consistently served as a vital platform for discussing the most challenging economic issues of the day. Judging by the agenda and the papers, this year will be no exception.

For the past year and a half, my colleagues and I on the Federal Open Market Committee (FOMC) have been conducting the first-ever public review of our monetary policy framework.1 Earlier today we released a revised Statement on Longer-Run Goals and Monetary Policy Strategy, a document that lays out our goals, articulates our framework for monetary policy, and serves as the foundation for our policy actions.2 Today I will discuss our review, the changes in the economy that motivated us to undertake it, and our revised statement, which encapsulates the main conclusions of the review.

Evolution of the Fed's Monetary Policy Framework

We began this public review in early 2019 to assess the monetary policy strategy, tools, and communications that would best foster achievement of our congressionally assigned goals of maximum employment and price stability over the years ahead in service to the American people. Because the economy is always evolving, the FOMC's strategy for achieving its goals—our policy framework—must adapt to meet the new challenges that arise. Forty years ago, the biggest problem our economy faced was high and rising inflation.3 The Great Inflation demanded a clear focus on restoring the credibility of the FOMC's commitment to price stability. Chair Paul Volcker brought that focus to bear, and the "Volcker disinflation," with the continuing stewardship of Alan Greenspan, led to the stabilization of inflation and inflation expectations in the 1990s at around 2 percent. The monetary policies of the Volcker era laid the foundation for the long period of economic stability known as the Great Moderation. This new era brought new challenges to the conduct of monetary policy. Before the Great Moderation, expansions typically ended in overheating and rising inflation. Since then, prior to the current pandemic-induced downturn, a series of historically long expansions had been more likely to end with episodes of financial instability, prompting essential efforts to substantially increase the strength and resilience of the financial system.4

By the early 2000s, many central banks around the world had adopted a monetary policy framework known as inflation targeting.5 Although the precise features of inflation targeting differed from country to country, the core framework always articulated an inflation goal as a primary objective of monetary policy. Inflation targeting was also associated with increased communication and transparency designed to clarify the central bank's policy intentions. This emphasis on transparency reflected what was then a new appreciation that policy is most effective when it is clearly understood by the public. Inflation-targeting central banks generally do not focus solely on inflation: Those with "flexible" inflation targets take into account economic stabilization in addition to their inflation objective.

Under Ben Bernanke's leadership, the Federal Reserve adopted many of the features associated with flexible inflation targeting.6 We made great advances in transparency and communications, with the initiation of quarterly press conferences and the Summary of Economic Projections (SEP), which comprises the individual economic forecasts of FOMC participants. During that time, then–Board Vice Chair Janet Yellen led an effort on behalf of the FOMC to codify the Committee's approach to monetary policy. In January 2012, the Committee issued its first Statement on Longer-Run Goals and Monetary Policy Strategy, which we often refer to as the consensus statement. A central part of this statement was the articulation of a longer-run inflation goal of 2 percent.7 Because the structure of the labor market is strongly influenced by nonmonetary factors that can change over time, the Committee did not set a numerical objective for maximum employment. However, the statement affirmed the Committee's commitment to fulfilling both of its congressionally mandated goals. The 2012 statement was a significant milestone, reflecting lessons learned from fighting high inflation as well as from experience around the world with flexible inflation targeting. The statement largely articulated the policy framework the Committee had been following for some time.8

Motivation for the Review

The completion of the original consensus statement in January 2012 occurred early on in the recovery from the Global Financial Crisis, when notions of what the "new normal" might bring were quite uncertain. Since then, our understanding of the economy has evolved in ways that are central to monetary policy. Of course, the conduct of monetary policy has also evolved. A key purpose of our review has been to take stock of the lessons learned over this period and identify any further changes in our monetary policy framework that could enhance our ability to achieve our maximum-employment and price-stability objectives in the years ahead.9

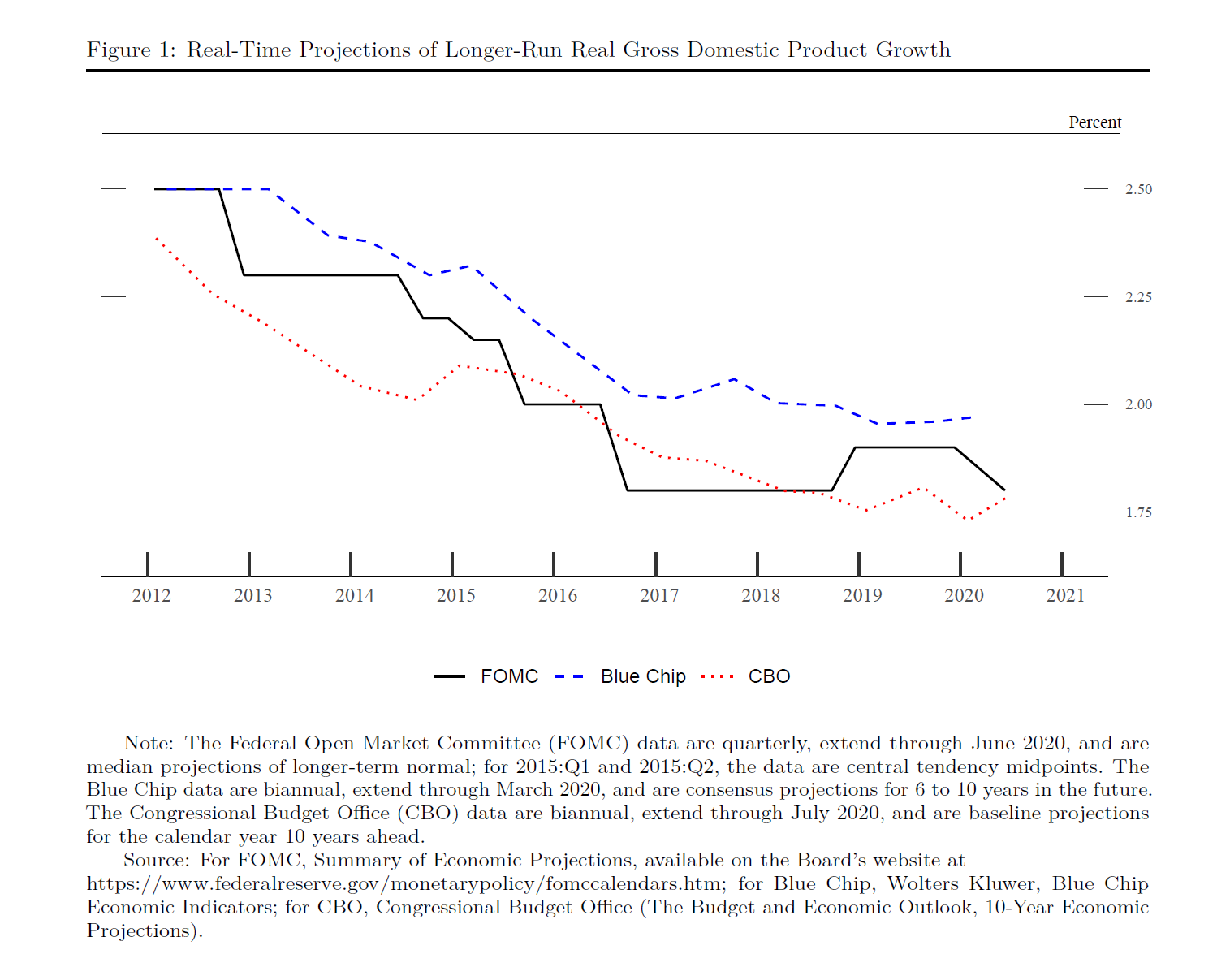

Our evolving understanding of four key economic developments motivated our review. First, assessments of the potential, or longer-run, growth rate of the economy have declined. For example, since January 2012, the median estimate of potential growth from FOMC participants has fallen from 2.5 percent to 1.8 percent (see figure 1). Some slowing in growth relative to earlier decades was to be expected, reflecting slowing population growth and the aging of the population. More troubling has been the decline in productivity growth, which is the primary driver of improving living standards over time.10

{kind=link}

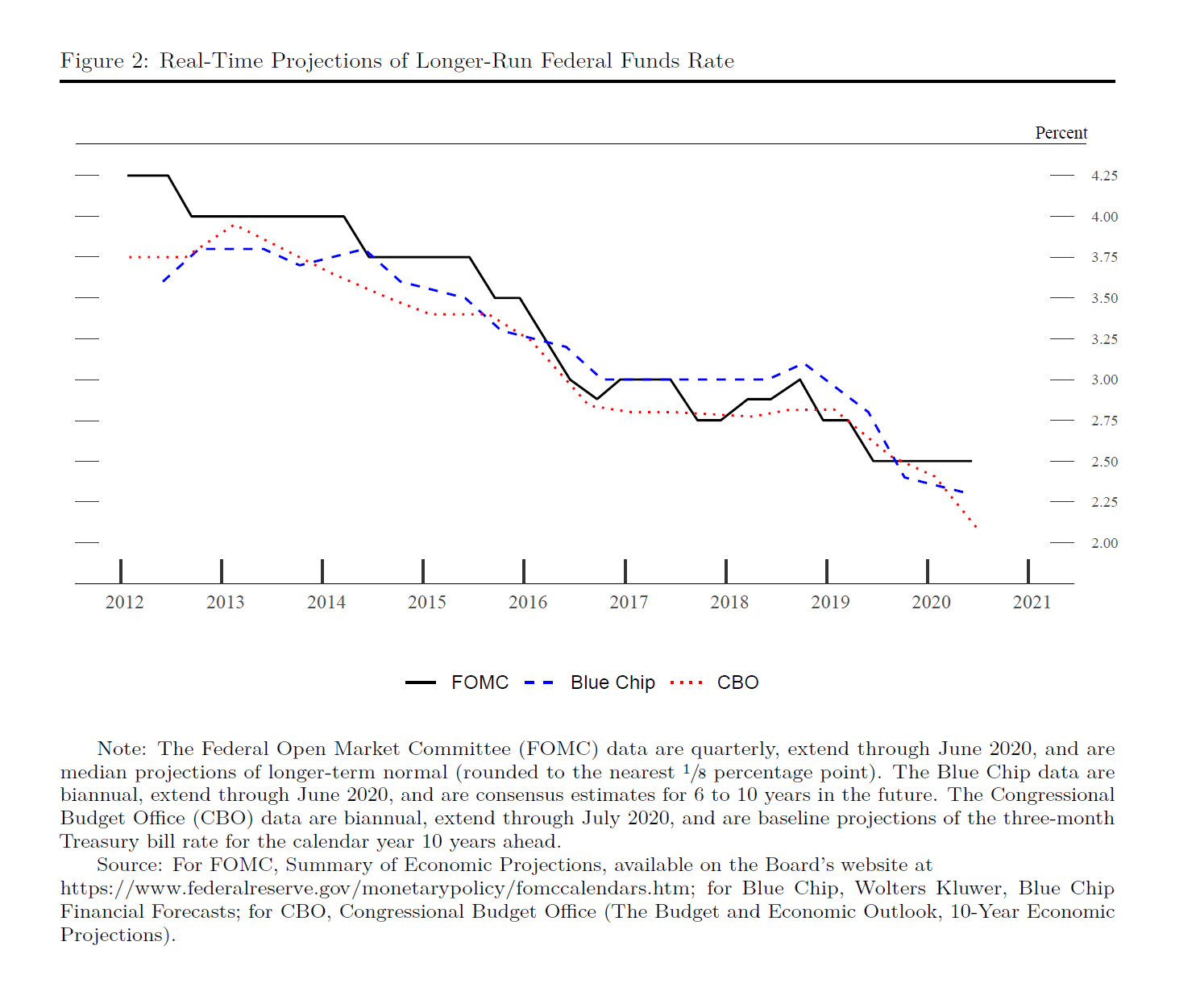

Second, the general level of interest rates has fallen both here in the United States and around the world. Estimates of the neutral federal funds rate, which is the rate consistent with the economy operating at full strength and with stable inflation, have fallen substantially, in large part reflecting a fall in the equilibrium real interest rate, or "r-star." This rate is not affected by monetary policy but instead is driven by fundamental factors in the economy, including demographics and productivity growth—the same factors that drive potential economic growth.11 The median estimate from FOMC participants of the neutral federal funds rate has fallen by nearly half since early 2012, from 4.25 percent to 2.5 percent (see figure 2).

{kind=link}

This decline in assessments of the neutral federal funds rate has profound implications for monetary policy. With interest rates generally running closer to their effective lower bound even in good times, the Fed has less scope to support the economy during an economic downturn by simply cutting the federal funds rate.12 The result can be worse economic outcomes in terms of both employment and price stability, with the costs of such outcomes likely falling hardest on those least able to bear them.

Pages: 1 · 2

More Articles

- Chair Jerome H. Powell Remarks at the Stanford Business, Government and Society Forum

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022

- Reflections on Monetary Policy in 2021 By Federal Reserve Governor Christopher J. Waller or "How did the Fed get so far behind the curve?"

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Prices are Spiking for Homes, Cars and Gas; Don’t Be Alarmed, Economists Say

- Federal Reserve Chair Jerome H. Powell: Building on the Gains from the Long Expansion: Spreading the Benefits of Employment