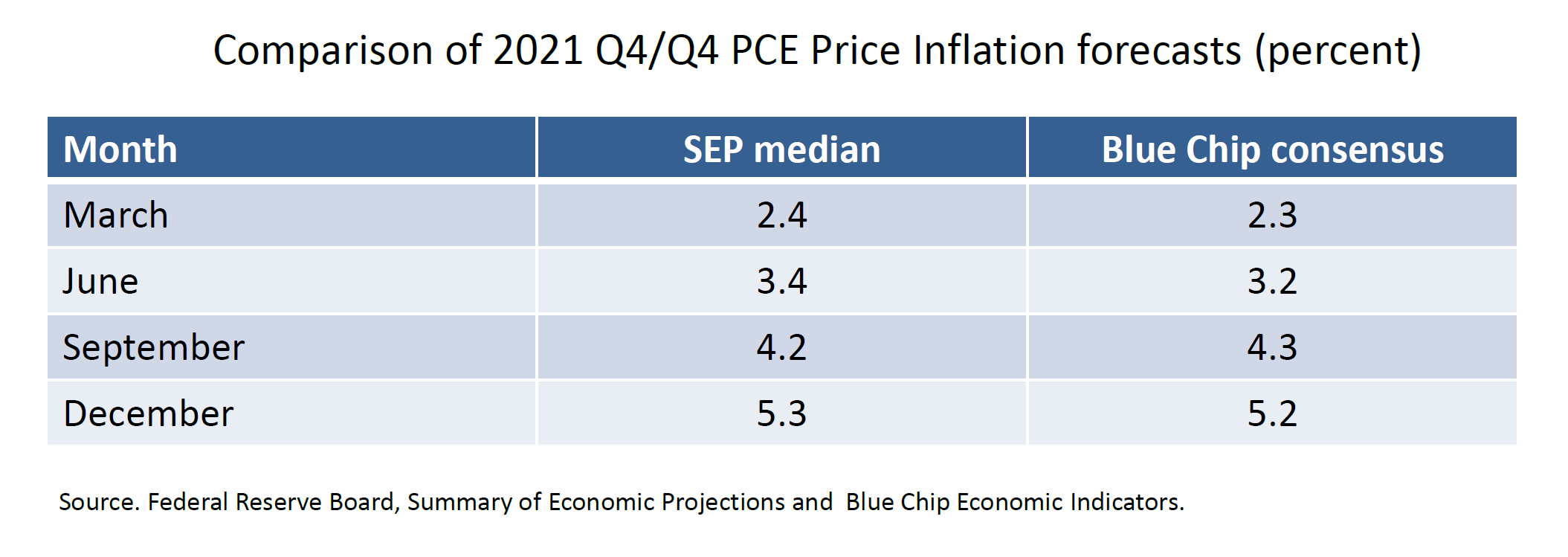

First, I want to emphasize that forecasting is hard for everyone, especially in a pandemic. In terms of missing on inflation, policymakers' projections looked very much like most of the public's. For example, as shown in table 1, the median SEP forecast for 2021 Q4/Q4 PCE inflation was very similar to the consensus from the Blue Chip, which is a compilation of private sector forecasts. In short, nearly everyone was behind the curve when it came to forecasting the magnitude and persistence of inflation.

{kind=link}

Second, as I mentioned, you cannot answer this question without taking a stand on the employment leg of our mandate. There was a clear difference in views on this and on what indicators should be looked at to determine whether we had met the 'substantial further progress" criteria we laid out in our December 2020 guidance. Some of us concluded the labor market was healing fast and we pushed for earlier and faster withdrawal of accommodation. For others, data suggested the labor market was not healing that fast and it was not optimal to withdraw policy accommodation soon. Many of our critics tend to focus only on the inflation aspect of our mandate and ignore the employment leg of our mandate. But we cannot. So, what may appear as a policy error to some was viewed as appropriate policy by others based on their views regarding the health of the labor market.

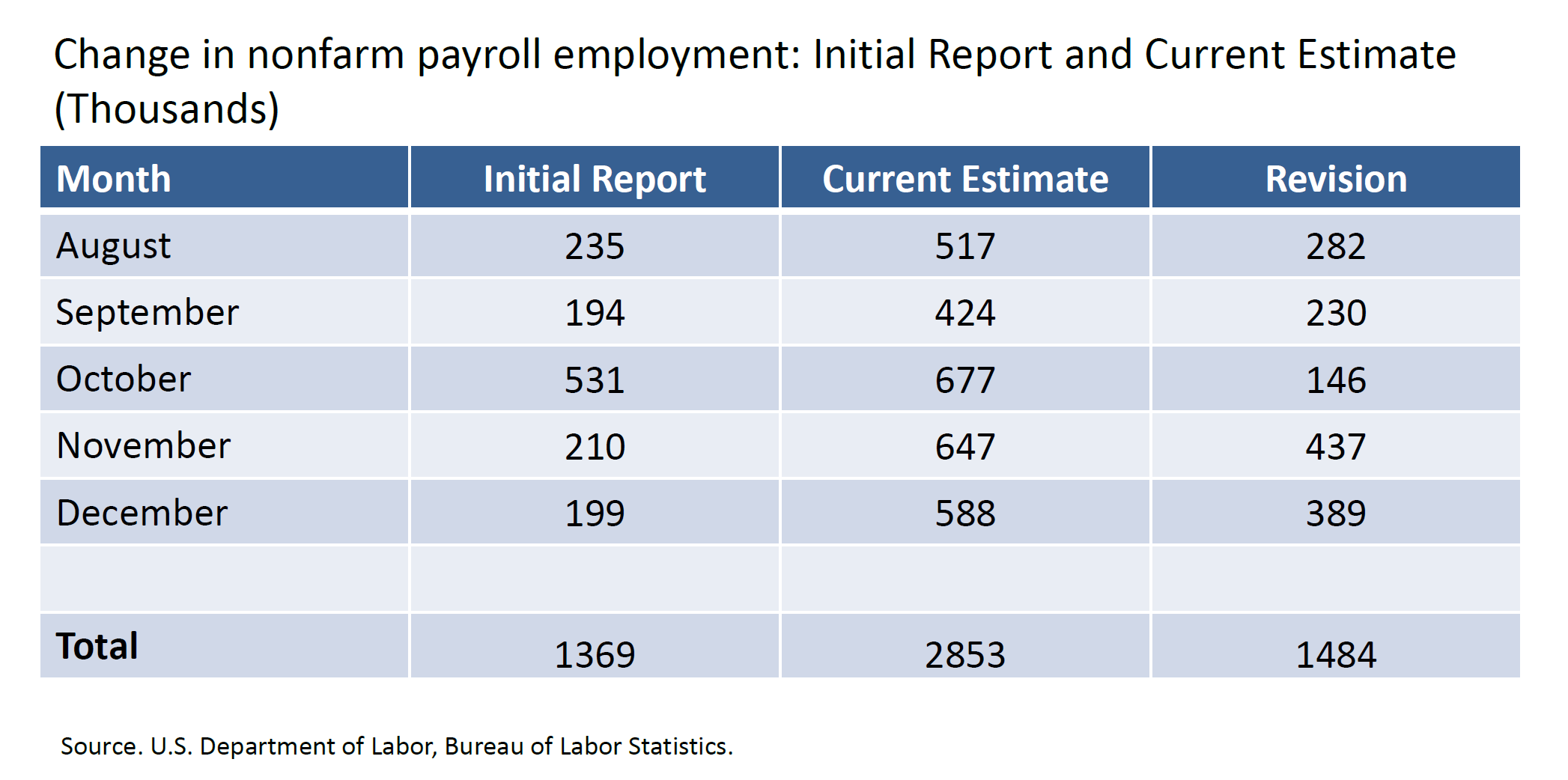

Third, one must account for setting policy in real time. The Committee was getting mixed signals from the labor market data in August and September. Two consecutive weak job reports didn't square with a rapidly falling unemployment rate. Later that fall, and then with the Labor Department's 2021 revisions, we found that payrolls were quite steady over the course of the year. As shown in table 2, revisions to changes in payroll employment since late last summer have been quite substantial. From the original reports to the current estimate, the change in payroll employment has been revised up nearly 1.5 million. As the revisions came in, a consensus grew that the labor market was much stronger than we originally thought. If we knew then what we know now, I believe the Committee would have accelerated tapering and raised rates sooner. But no one knew, and that's the nature of making monetary policy in real time.

{kind=link}

Finally, if one believes we were behind the curve in 2021, how far behind were we? In a world of forward guidance, one simply cannot look at the policy rate to judge the stance of policy. Even though we did not actually move the policy rate in 2021, we used forward guidance to start raising market rates starting with the September 2021 statement, which indicated tapering was coming soon. The 2-year Treasury yield, which I view as a good market indicator of our policy stance, went from approximately 25 basis points in late September 2021 to 75 basis points by late December. That is the equivalent, in my mind, of two 25 basis point policy rate hikes for impacting the financial markets. When looked at this way, how far behind the curve could we have possibly been if, using forward guidance, one views rate hikes effectively beginning in September 2021?

1. See Jeff Cox (2021), "Fed's Waller Says the Economy Is 'Ready to Rip' But Policy Should Stay Put," CNBC, April 16. Return to text

2. See Christopher J. Waller (2021), "A Hopeless and Imperative Endeavor: Lessons from the Pandemic for Economic Forecasters," speech delivered at the Forecasters Club of New York, New York, December 17. Return to text

3. See Board of Governors of the Federal Reserve System (2021), "Minutes of the Federal Open Market Committee, June 15–16, 2021," press release. Return to text

4. See Board of Governors of the Federal Reserve System (2021), "Minutes of the Federal Open Market Committee, July 27–28, 2021," press release. Return to text

5. See Ann Saphir (2021), "Fed's Waller: 'Go Early and Go Fast' on Taper," Reuters, August 2. Return to text

6. Of course, as we all know, these employment data would be revised upward substantially, but that was not known to policymakers at the time, and it's important to explicitly make that point now—the data were choppy and did not lend themselves to a clear picture of the outlook. Return to text

7. See Board of Governors of the Federal Reserve System (2021), "FOMC Statement," press release, September 22. Return to text

8. See Board of Governors of the Federal Reserve System (2021), "FOMC Statement," press release, November 3. Return to text

Pages: 1 · 2

More Articles

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022

- Federal Reserve Chairman Jerome Powell: Monetary Policy in the Time of Covid

- Prices are Spiking for Homes, Cars and Gas; Don’t Be Alarmed, Economists Say

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- New Economic Challenges and the Fed's Monetary Policy Review by Chair of the Federal Reserve Jerome H. Powell

- Federal Reserve Chair Jerome H. Powell: Building on the Gains from the Long Expansion: Spreading the Benefits of Employment