For the Federal Reserve, the answer to this question has important implications for monetary policy. If the current, elevated rate of unemployment is largely cyclical, then the straightforward solution is to take action to raise aggregate demand. If unemployment is instead substantially structural, some worry that attempts to raise aggregate demand will have little effect on unemployment and serve only to stoke inflation.

This question is frequently discussed by the FOMC.12 I cannot speak for the Committee or my colleagues, some of whom have publicly related their own conclusions on this topic. However, I see the evidence as consistent with the view that the increase in unemployment since the onset of the Great Recession has been largely cyclical and not structural.

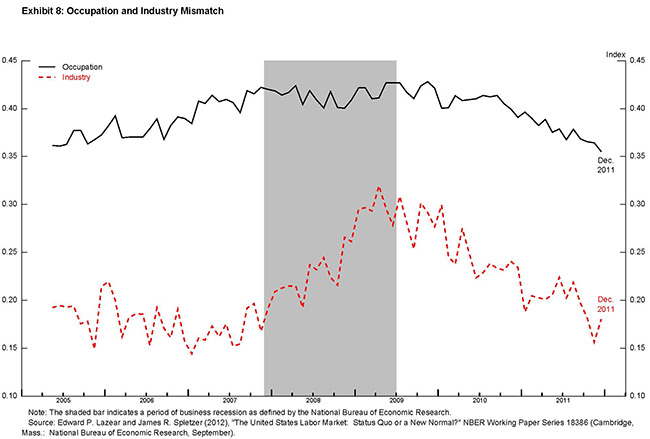

For example, the rise in unemployment during the recession was accompanied by a dramatic decline in job vacancies and was widespread across industry and occupation groups. Job losses in the construction and financial services industries were particularly large — hardly surprising given the collapse in these sectors in 2008 and 2009 — but manufacturing and other cyclically sensitive industries were hit hard as well, and employment in these industries has likewise recovered slowly. Moreover, if skills mismatch in the labor market has led to an excess supply of workers in some sectors and a shortage of workers in others, then we would expect to see an atypical amount of variation in the balance between job openings and unemployment across sectors. Based on this insight, researchers Ed Lazear and Jim Spletzer constructed quantitative measures of mismatch across industries and occupations.13 They found that their mismatch indexes were indeed elevated at the end of the Great Recession, as exhibit 8 shows. But these measures have fallen over the course of the recovery to near pre-recession levels. In addition, widespread mismatch between job vacancies and workers across different sectors might be expected to cause wage rates to rise relatively quickly in sectors with many job openings and relatively slowly in sectors with an excess supply of available workers. But work by Jesse Rothstein fails to uncover evidence of such a pattern.14

{kind=link}

This and related research suggests to me, first, that a broad-based cyclical shortage of demand is the main cause of today's elevated unemployment rate, and, second, that whatever problems there may be today with labor market functioning are likely to be substantially resolved as the broader economy improves and bolsters the demand for labor.

I don't mean to suggest that there aren't some workers who have been stranded by structural changes in the economy. More can and should be done to help dislocated workers acquire new skills to transition from industries and occupations with fewer opportunities. But making this transition will be much easier in a healthy economy, which is one reason why I am encouraged by the evidence that elevated unemployment is indeed largely cyclical. I will now describe what the Federal Reserve is doing to try to raise demand and create jobs.

I have described the two unconventional policy tools that the FOMC has employed since it reduced the target federal funds rate in 2008 to its effective lower bound. The first is large-scale asset purchases, intended to lower long-term interest rates to encourage borrowing for spending and investment. Between 2008 and mid-2011, the FOMC purchased agency-guaranteed mortgage-backed securities (MBS), agency debt, and Treasury securities totaling $2.3 trillion. In 2011, the FOMC began the maturity extension program, under which it reduced its holdings of short-term Treasury securities and used the proceeds to purchase an equivalent amount of longer-term Treasury securities.

However, as the scheduled endpoint of that program approached, it became clear that the economy remained weak, and the FOMC took a series of steps to provide further impetus to the recovery. In June 2012, the Committee extended its maturity extension program until the end of the year. Then in September, it made a major new commitment to asset purchases. Unlike its past purchase programs, which were fixed in size, this time the FOMC stated its determination to continue the program, provided that inflation remains well contained, until it judges that there has been a substantial improvement in the outlook for the labor market. The Committee currently intends to purchase MBS and Treasury debt at a pace that will add about $85 billion per month of such securities to the Federal Reserve's balance sheet. In determining the size, pace, and composition of these purchases over time, the Committee will also take into account ongoing assessments of their efficacy and costs.

The second unconventional policy tool that the FOMC has used is forward guidance, in the form of more-explicit and more-detailed information about the future path of monetary policy. The longer-term interest rates that most profoundly influence housing demand, capital spending, and asset prices depend on current and expected future levels of short-term interest rates, such as the federal funds rate that has been the Fed's conventional monetary policy tool. Signaling the future path of the federal funds rate can therefore directly affect interest rates today on auto loans, home mortgages, and bonds issued by companies and state and local governments, even when the current level of the federal funds rate cannot be lowered.

The FOMC has substantially expanded its forward guidance in recent years. In 2009, the Committee stated that economic conditions "are likely to warrant exceptionally low levels of the federal funds rate for an extended period."15 In 2011, the FOMC said this period would likely last "at least through mid-2013," and extended this date guidance several times.16

A disadvantage of this calendar-based approach was that it might not be clear whether changes in the date reflect changes in the FOMC's outlook for growth, for inflation, or a shift in the desired stance of policy. In December 2012, the FOMC therefore replaced the date with greater detail on the economic conditions that would warrant maintaining the federal funds rate at its present, exceptionally low level. Specifically, it stated that near-zero rates would likely remain appropriate for a considerable time after the asset purchase program ends and "at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee's 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored."17

It deserves emphasis that a 6-1/2 percent unemployment rate and inflation one to two years ahead that is 1/2 percentage point above the Committee's 2 percent objective are thresholds for possible action, not triggers that will necessarily prompt an immediate increase in the FOMC's target rate. In practical terms, it means that the Committee does not expect to raise the federal funds rate as long as unemployment remains above 6-1/2 percent and inflation one to two years ahead is projected to be less than 1/2 percentage point above its 2 percent objective. When one of these thresholds is crossed, action is possible but not assured.

Moreover, these thresholds for possible action do not reflect any change in the Committee's longer-run goals. With respect to maximum employment, most FOMC participants continue to estimate that the longer-run normal unemployment rate lies in a range of 5.2 to 6 percent, and the Committee continues to believe an inflation rate of 2 percent (as measured by the annual change in the price index for personal consumption expenditures) is most consistent with the Federal Reserve's dual mandate. Indeed, the Committee reaffirmed these longer-run goals, first adopted in January 2012, just last month.18 Of course, our control over the economy is imperfect, and so temporary deviations from the FOMC's specific longer-term goals will sometimes occur. Importantly, these quantitative goals are neither ceilings nor floors for inflation and unemployment, and the Committee will take a balanced approach to returning both measures to their objectives over time.

I believe the policy steps we have taken recently are in accord with this balanced approach. With employment so far from its maximum level and with inflation currently running, and expected to continue to run, at or below the Committee's 2 percent longer-term objective, it is entirely appropriate for progress in attaining maximum employment to take center stage in determining the Committee's policy stance.

While the Committee's longer-term goals remain unchanged, what has changed is that the FOMC is now providing more information about how it expects to pursue its inflation and employment goals. In particular, we will employ our policy tools, as appropriate, to raise aggregate demand and employment in the context of continued price stability, consistent with our balanced approach. That's good news for workers, because I believe that these steps will increase demand, and more demand means more jobs.

It will be a long road back to a healthy job market. It will be years before many workers feel like they have regained the ground lost since 2007. Longer-term trends, such as globalization and technological change, will continue to pose challenges to workers in many industries.

Let me close with some words of encouragement. The job market is improving. The progress has been too slow, but there is progress. My colleagues and I at the Federal Reserve are well aware of the difficulties faced by workers in this slow recovery, and we're actively engaged in continuing efforts to promote a stronger economy, more jobs, and better conditions for all workers.

Thank you for the opportunity to speak to you today.

More Articles

- Federal Reserve Issues A Federal Open Market Committee Statement: Committee Will Aim to Achieve Inflation Moderately Above 2% For Some Time

- Biden-Harris Administration Marks Anniversary of Americans with Disabilities Act and Announces Resources to Support Individuals with Long COVID, Increased Access to Democracy for Voters with Disabilities

- Coronavirus Aid, Relief, and Economic Security Act; Chair Jerome H. Powell Before the Committee on Financial Services, House of Representatives

- Jo Freeman Reviews Stories from Trailblazing Women Lawyers: Lives in the Law by Jill Norgren

- Chair Jerome H. Powell: A Current Assessment of the Response to the Economic Fallout of this Historic Event

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- Supreme Court Surprises The Public in LGBTQ Ruling: What is Sex Discrimination?

- The Outlook for Housing: Federal Reserve Governor Michelle W. Bowman at the 2020 Economic Forecast Breakfast

- Weekly Legislative Update: Pregnant Worker Fairness Act, Runaway and Homeless Youth and Trafficking Preventing Act and Congressional Bills Introduced

- The Uber and Lyft of Dog Walking Fight State Oversight