In trying to account for why this recovery has been so weak, it is helpful to first consider several important factors that have in the past supported most economic recoveries. By this I don't mean everything that contributes to economic growth, but rather those things that typically play a key role when the US economy is recovering from recession. Think of these as the tailwinds that usually promote a recovery.

The first tailwind I'll mention is fiscal policy. History shows that fiscal policy often helps to support an economic recovery. Some of this fiscal stimulus is automatic, and intended to be. The income loss that individuals and businesses suffer in a recession is partly offset when their tax bills fall as well. Government spending on unemployment benefits and other safety-net programs rises in recessions, helping individuals hurt by the downturn and also supporting consumer spending and the broader economy by replacing lost income. These automatic declines in tax collections and increases in government spending are often supplemented with discretionary fiscal action — tax rate cuts, spending on infrastructure and other goods and services, and extended unemployment benefits. These discretionary fiscal policy actions are typically a plus for growth in the years just after a recession. For example, following the severe 1981-82 recession, discretionary fiscal policy contributed an average of about 1 percentage point per year to real GDP growth over the subsequent three years.5

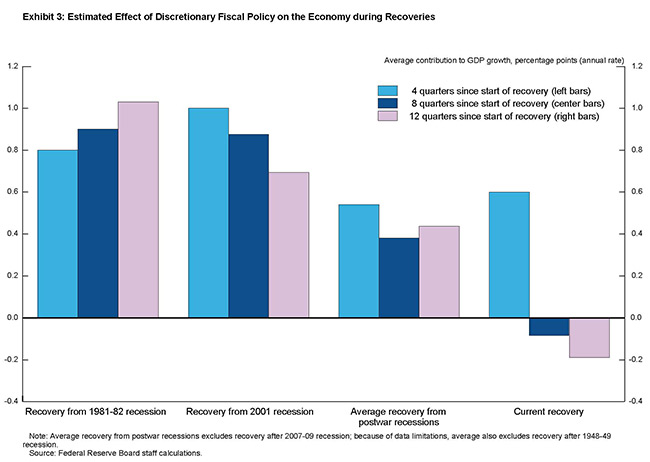

However, discretionary fiscal policy hasn't been much of a tailwind during this recovery. In the year following the end of the recession, discretionary fiscal policy at the federal, state, and local levels boosted growth at roughly the same pace as in past recoveries, as exhibit 3 indicates. But instead of contributing to growth thereafter, discretionary fiscal policy this time has actually acted to restrain the recovery. State and local governments were cutting spending and, in some cases, raising taxes for much of this period to deal with revenue shortfalls. At the federal level, policymakers have reduced purchases of goods and services, allowed stimulus-related spending to decline, and have put in place further policy actions to reduce deficits. I was relieved that the Congress and the Administration were able to reach agreement on avoiding the full force of the "fiscal cliff" that was due to take effect on January 1. While a long-term plan is needed to reduce deficits and slow the growth of federal debt, the tax increases and spending cuts that would have occurred last month, absent action by the Congress and the President, likely would have been a headwind strong enough to blow the United States back into recession. Negotiations continue over the extent of spending cuts now due to take effect beginning in March, and I expect that discretionary fiscal policy will continue to be a headwind for the recovery for some time, instead of the tailwind it has been in the past.

{kind=link}

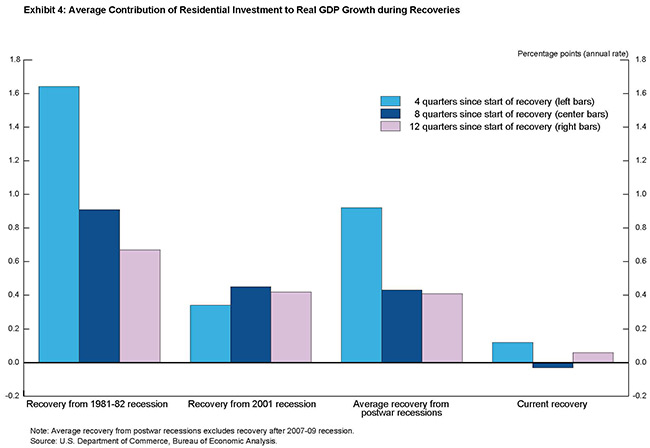

A second tailwind in most recoveries is housing. Residential investment creates jobs in construction and related industries. Before the Great Recession, housing investment added an average of 1/2 percentage point to real GDP growth in the two years after each of the previous four recessions, considerably more than its contribution to growth at other times.6

During this recovery, in contrast, residential investment, on net, has contributed very little to growth since the recession ended. The reasons are easy to understand, given the central role that housing played in the Great Recession. Following an extended boom in construction driven in large part by overly loose mortgage lending standards and unrealistic expectations for future home price increases, the housing market collapsed — sales and prices plunged and mortgage credit was sharply curtailed. Tight mortgage credit conditions are continuing to make it difficult for many families to buy homes, despite record-low mortgage interest rates that have helped make housing very affordable. I'm encouraged by recent improvement in the residential sector, but the contribution of housing investment to overall economic activity remains considerably below the average seen in past recoveries, as exhibit 4 shows.

{kind=link}

Beyond the direct effects on residential investment, the extraordinary collapse in house prices resulted in a huge loss of household wealth — at last count, net home equity is still down 40 percent, or about $5 trillion, from 2005.7 This loss of wealth has weighed on the finances and spending of many homeowners. Households are less able to tap their home equity to deal with economic shocks, fund their children's education, or start new businesses. For some hou seholds, the collapse in house prices has left them underwater on their mortgages, and thus less able to refinance or sell their homes.

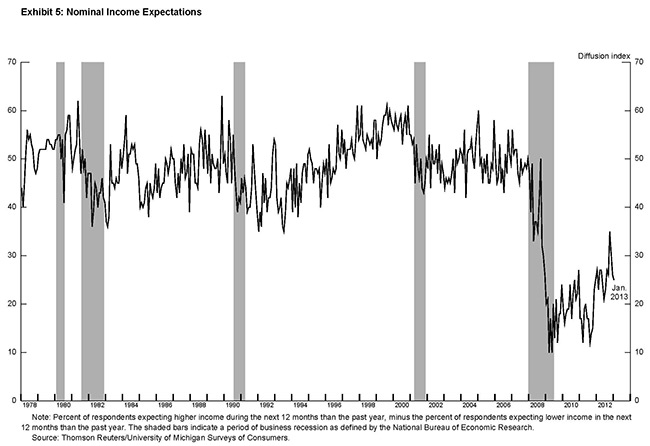

Another important tailwind in most economic recoveries is one that tends to be taken for granted — the faith most of us have, based on history and personal experience, that recessions are temporary and that the economy will soon get back to normal. Even during recessions, households' expectations for income growth tend to be reasonably stable, which provides support for overall spending. In the most recent recession, however, surveys suggest that consumers sharply revised down their prospects for future income growth and have only partially adjusted up their expectations since then (exhibit 5).

{kind=link}

The recovery has also encountered some unusual headwinds. The fiscal and financial crisis in Europe has resulted in a euro-area recession and contributed to slower global growth. Europe's difficulties have blunted what had been strong growth in US exports earlier in the recovery by sapping demand worldwide.

Let me say a few words now, and more later, about the role of monetary policy in this recovery. The Federal Reserve typically plays a large role in promoting recoveries by reducing the federal funds rate and keeping it low until the economy is again on a solid footing. Reducing the federal funds rate tends to reduce other interest rates and boost asset prices, thus encouraging spending and investment throughout the economy.

As it has before, the Federal Open Market Committee (FOMC) in 2007 started reducing the federal funds rate at the first signs of economic weakness and made sharper rate cuts as the recession deepened. As in some past recoveries that were disappointingly slow, the FOMC has kept rates low well after the end of the recession.

But unlike the past, by December 2008 the Committee had reduced the federal funds rate effectively to zero. Because that rate, for practical purposes, cannot be cut further, this level is referred to as the effective lower bound. Without the option of using its conventional policy tool, and with the recession getting worse, the FOMC decided to employ unconventional tools to further ease monetary policy, even though the efficacy of these tools was uncertain and it was recognized that their use might carry some potential costs. The better known of these tools is the purchase of large amounts of longer-term government securities, which is commonly referred to as quantitative easing. The other unconventional tool is known as forward guidance — providing information about the future path of short-term interest rates anticipated by the Committee. Both of these approaches are intended to address a gap caused by the effective lower bound. This gap is the shortfall between what the FOMC likely would do in current economic circumstances, were it able to reduce the federal funds rate below zero, and the reality that the rate can't be cut further.

I believe that the Federal Reserve's asset purchases and other unconventional policy actions have helped, and are continuing to help, fill this gap and thus shore up aggregate demand. The evidence suggests that the FOMC's actions have lowered short- and longer-term private borrowing rates and boosted asset prices.8 However, while this contribution has been significant, lower interest rates may be doing less to increase spending than in past recoveries because of some unusual features of the Great Recession and the current recovery. For example, as I noted, the housing crisis left many homeowners with high loan-to-value ratios and damaged credit records, creating barriers to their access to credit, while the financial crisis led many banks to lend only to borrowers with higher credit scores. As a consequence, the proportion of households that have been able to take advantage of declining rates to refinance their mortgages or to borrow to purchase new homes has probably been lower than in past recoveries. In addition, pronounced uncertainty about economic conditions has weighed on capital spending decisions and may have blunted the normal effect of lower interest rates on business investment.

These are the major reasons why I believe this recovery has been so slow. After a lengthy recession that imposed great hardships on American workers, the weak recovery has made the past five years the toughest that many of today's workers have ever experienced.

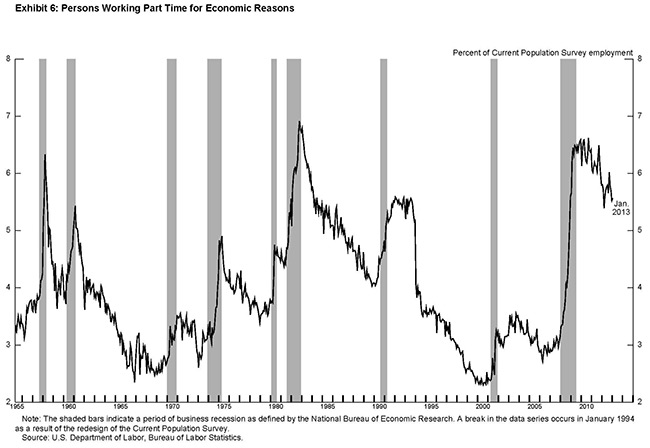

The unemployment rate now stands at 7.9 percent. To put this number in perspective, while that's a big improvement from the 10 percent reached in late 2009, it is now higher than unemployment ever got in the 24 years before the Great Recession. Moreover, the government's current estimate of 12 million unemployed doesn't include 800,000 discouraged workers who say they have given up looking for work. And, as exhibit 6 shows, 8 million people, or 5.6 percent of the workforce, say they are working part time even though they would prefer a full-time job. A broader measure of underemployment that includes these and other potential workers stands at 14.4 percent.

{kind=link}

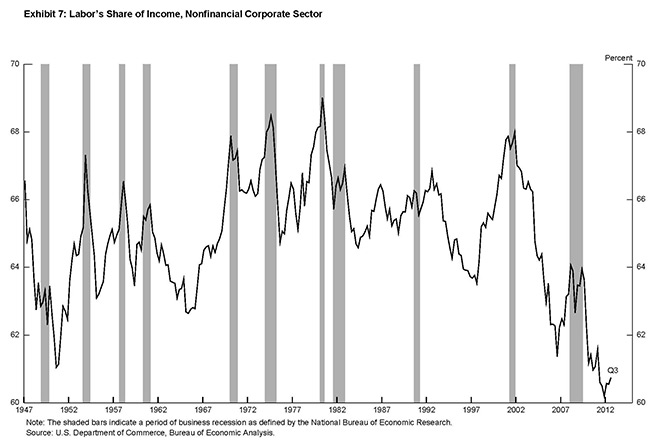

The effects of the recession and the subsequent slow recovery have been harshest on some of the most vulnerable Americans. The poverty rate has risen sharply since the onset of the recession, after a decade in which it had been relatively stable, and stands at 15 percent of the population, significantly above the average of the past three decades.9 Even those today who are fortunate enough to hold jobs have seen their hourly compensation barely keep pace with the cost of living over the past three years, while labor's share of income — as measured by the percent of production by nonfinancial corporations accruing to workers as compensation — remains near the postwar low reached in 2011 (exhibit 7). Compared with the 7.9 percent unemployment rate for all workers, the unemployment rate for African Americans is 13.8 percent. The unemployment rate for those without a high school diploma is 12 percent. For young people — workers 16 to 19 years old — the unemployment rate is 23.4 percent, little changed from the end of the recession. Among African Americans in that age group, 38 percent of those in the labor force can't find a job.

{kind=link}

Another gauge of the effect that this slow recovery has had on workers is how long it is taking to find a job. At its worst point in the 1980s, the median length of unemployment for those looking for a job was 12 weeks, but the median since the Great Recession has averaged 20 weeks and now stands at 16 weeks. Three million Americans have been looking for work for one year or more; that's one-fourth of all unemployed workers, which is down from 2011's peak but far larger than was seen before the Great Recession.

These are not just statistics to me. We know that long-term unemployment is devastating to workers and their families. Longer spells of unemployment raise the risk of homelessness and have been a factor contributing to the foreclosure crisis. When you're unemployed for six months or a year, it is hard to qualify for a lease, so even the option of relocating to find a job is often off the table. The toll is simply terrible on the mental and physical health of workers, on their marriages, and on their children.10

Long-term unemployment is also a great concern because it has the potential to itself become a headwind restraining the economy. Individuals out of work for an extended period can become less employable as they lose the specific skills acquired in their previous jobs and also lose the habits needed to hold down any job. Those out of work for a long time also tend to lose touch with former co-workers in their previous industry or occupation — contacts that can often help an unemployed worker find a job. Long-term unemployment can make any worker progressively less employable, even after the economy strengthens.

A factor contributing to the high level of long-term unemployment in the current recovery is the relatively large proportion of workers who have permanently lost their previous jobs, as opposed to being laid off temporarily. For example, in past recessions, a considerable share of jobs lost in construction has been temporary, but that isn't the case this time. Construction employment fell from its peak of 7.7 million in 2006 to a low of 5.4 million in 2011. Only about 300,000 of those 2.3 million jobs have returned and most won't, at least for many years.

In general, individuals who permanently lose their previous jobs take longer to become reemployed than do those on temporary layoff, are more likely to have to change industries or occupations to find a new job, and earn significantly less when they become reemployed.11

The greater amount of permanent job loss seen in the recent recession also suggests that there might have been an increase in the degree of mismatch between the skills possessed by the unemployed and those demanded by employers. This possibility and the unprecedented level and persistence of long-term unemployment in this recovery have prompted some to ask whether a significant share of unemployment since the recession is due to structural problems in labor markets and not simply a cyclical shortfall in aggregate demand. This question is important for anyone committed to the goal of maximum employment, because it implicitly asks whether the best we can hope for, even in a healthy economy, is an unemployment rate significantly higher than what has been achieved in the past.

More Articles

- Federal Reserve Issues A Federal Open Market Committee Statement: Committee Will Aim to Achieve Inflation Moderately Above 2% For Some Time

- Biden-Harris Administration Marks Anniversary of Americans with Disabilities Act and Announces Resources to Support Individuals with Long COVID, Increased Access to Democracy for Voters with Disabilities

- Coronavirus Aid, Relief, and Economic Security Act; Chair Jerome H. Powell Before the Committee on Financial Services, House of Representatives

- Jo Freeman Reviews Stories from Trailblazing Women Lawyers: Lives in the Law by Jill Norgren

- Chair Jerome H. Powell: A Current Assessment of the Response to the Economic Fallout of this Historic Event

- Federal Reserve: Optimism in the Time of COVID; Businesses Seem Much Better Adapted to Remaining Open

- Supreme Court Surprises The Public in LGBTQ Ruling: What is Sex Discrimination?

- The Outlook for Housing: Federal Reserve Governor Michelle W. Bowman at the 2020 Economic Forecast Breakfast

- Weekly Legislative Update: Pregnant Worker Fairness Act, Runaway and Homeless Youth and Trafficking Preventing Act and Congressional Bills Introduced

- The Uber and Lyft of Dog Walking Fight State Oversight