These late-breaking improvements in the labor market did not result in unwanted upward pressures on inflation, as might have been expected; in fact, inflation did not even rise to 2 percent on a sustained basis. There was every reason to expect that the labor market could have strengthened even further without causing a worrisome increase in inflation were it not for the onset of the pandemic.

The Labor Market Today

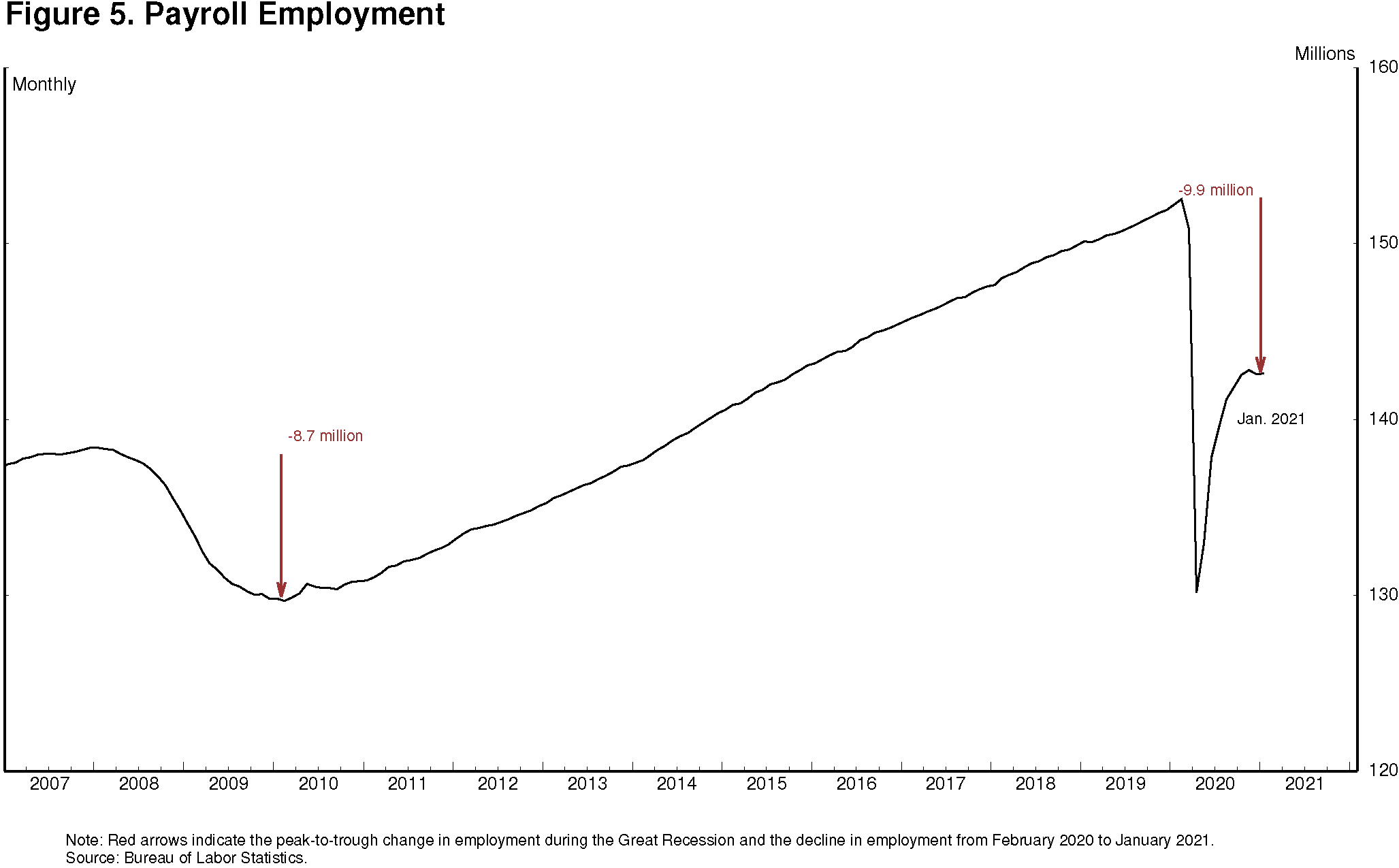

The state of our labor market today could hardly be more different. Despite the surprising speed of recovery early on, we are still very far from a strong labor market whose benefits are broadly shared. Employment in January of this year was nearly 10 million below its February 2020 level, a greater shortfall than the worst of the Great Recession's aftermath (figure 5).

{kind=link}

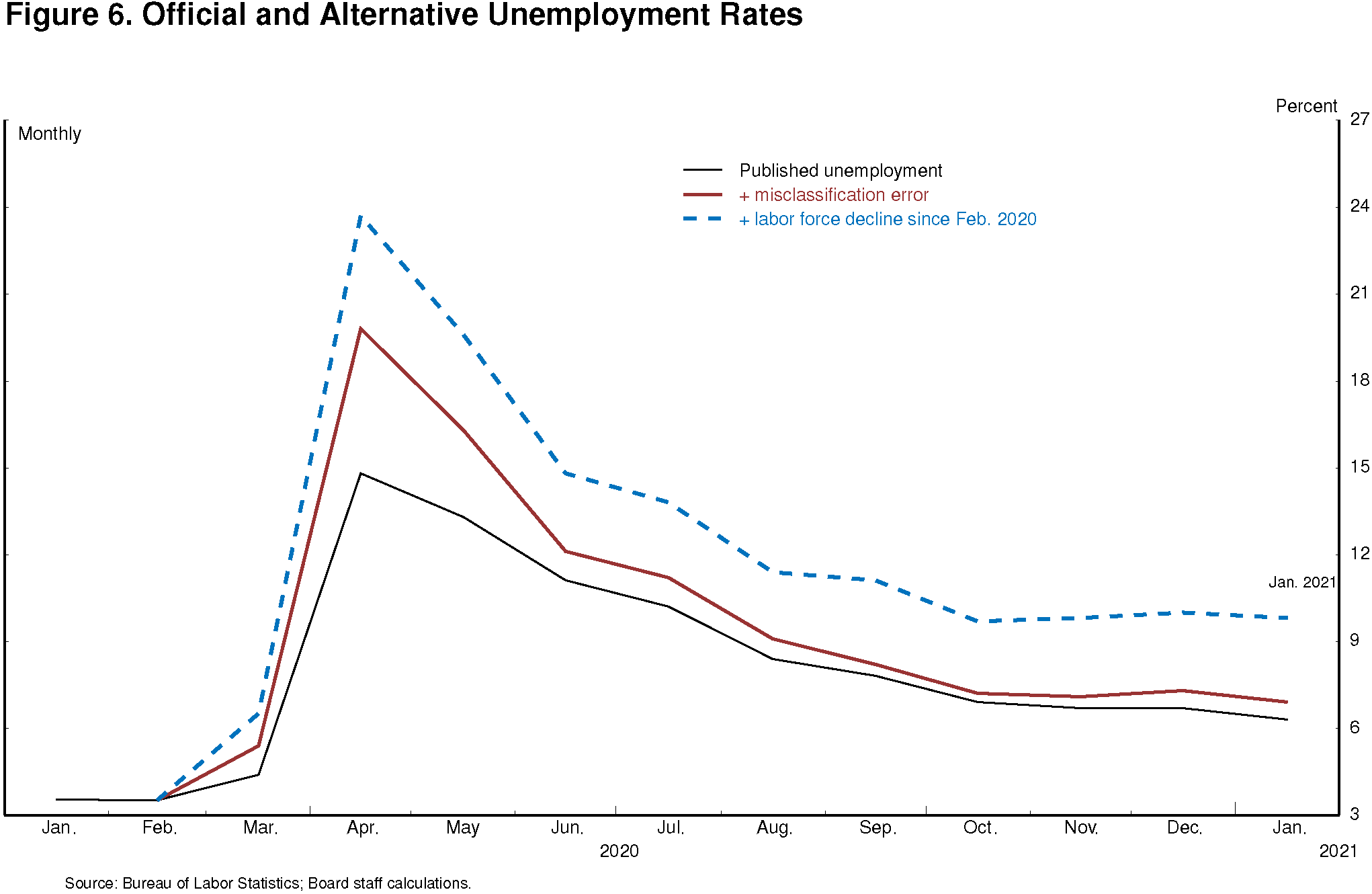

After rising to 14.8 percent in April of last year, the published unemployment rate has fallen relatively swiftly, reaching 6.3 percent in January. But published unemployment rates during COVID have dramatically understated the deterioration in the labor market. Most importantly, the pandemic has led to the largest 12-month decline in labor force participation since at least 1948.5 Fear of the virus and the disappearance of employment opportunities in the sectors most affected by it, such as restaurants, hotels, and entertainment venues, have led many to withdraw from the workforce. At the same time, virtual schooling has forced many parents to leave the work force to provide all-day care for their children. All told, nearly 5 million people say the pandemic prevented them from looking for work in January. In addition, the Bureau of Labor Statistics reports that many unemployed individuals have been misclassified as employed. Correcting this misclassification and counting those who have left the labor force since last February as unemployed would boost the unemployment rate to close to 10 percent in January (figure 6).

{kind=link}

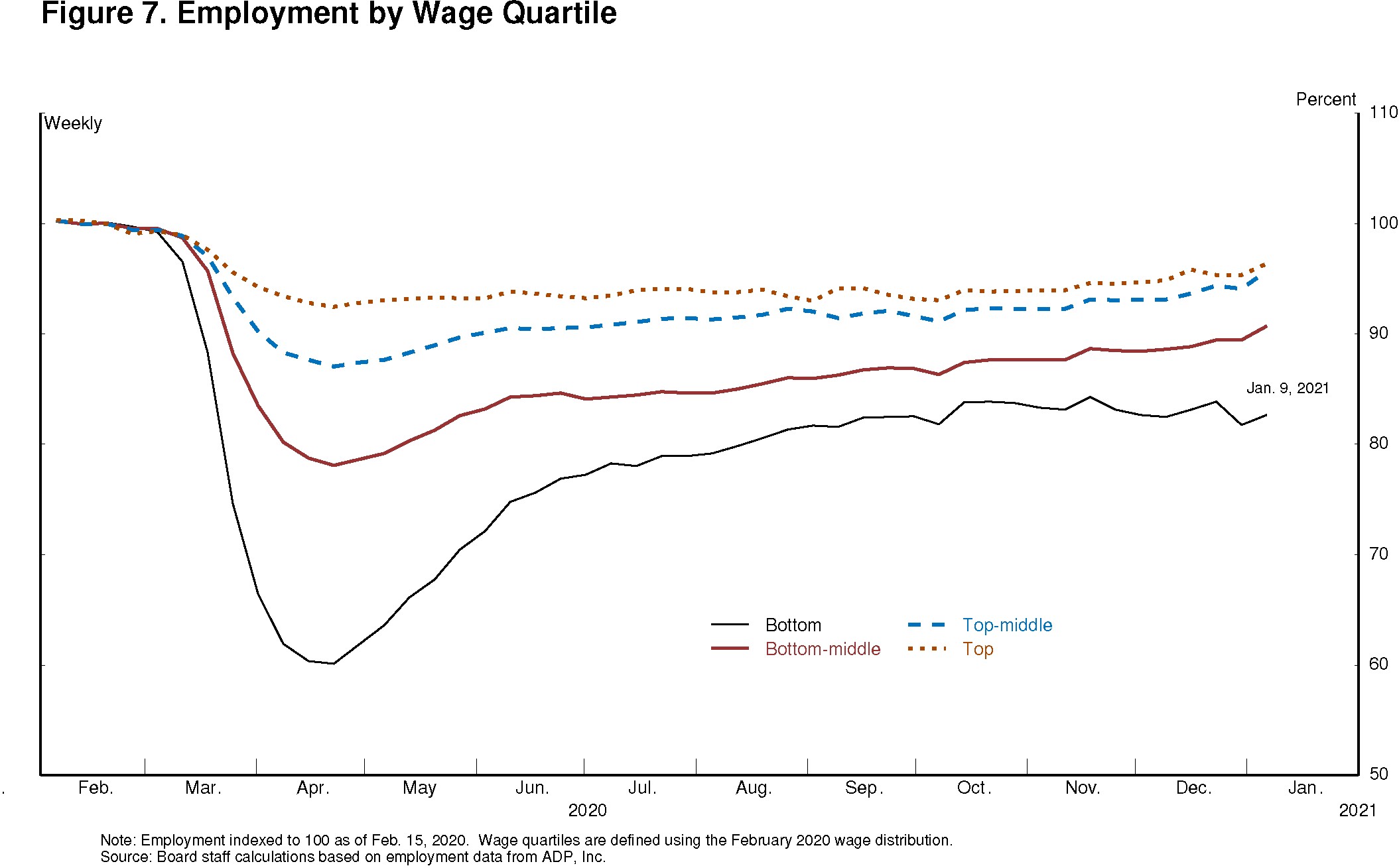

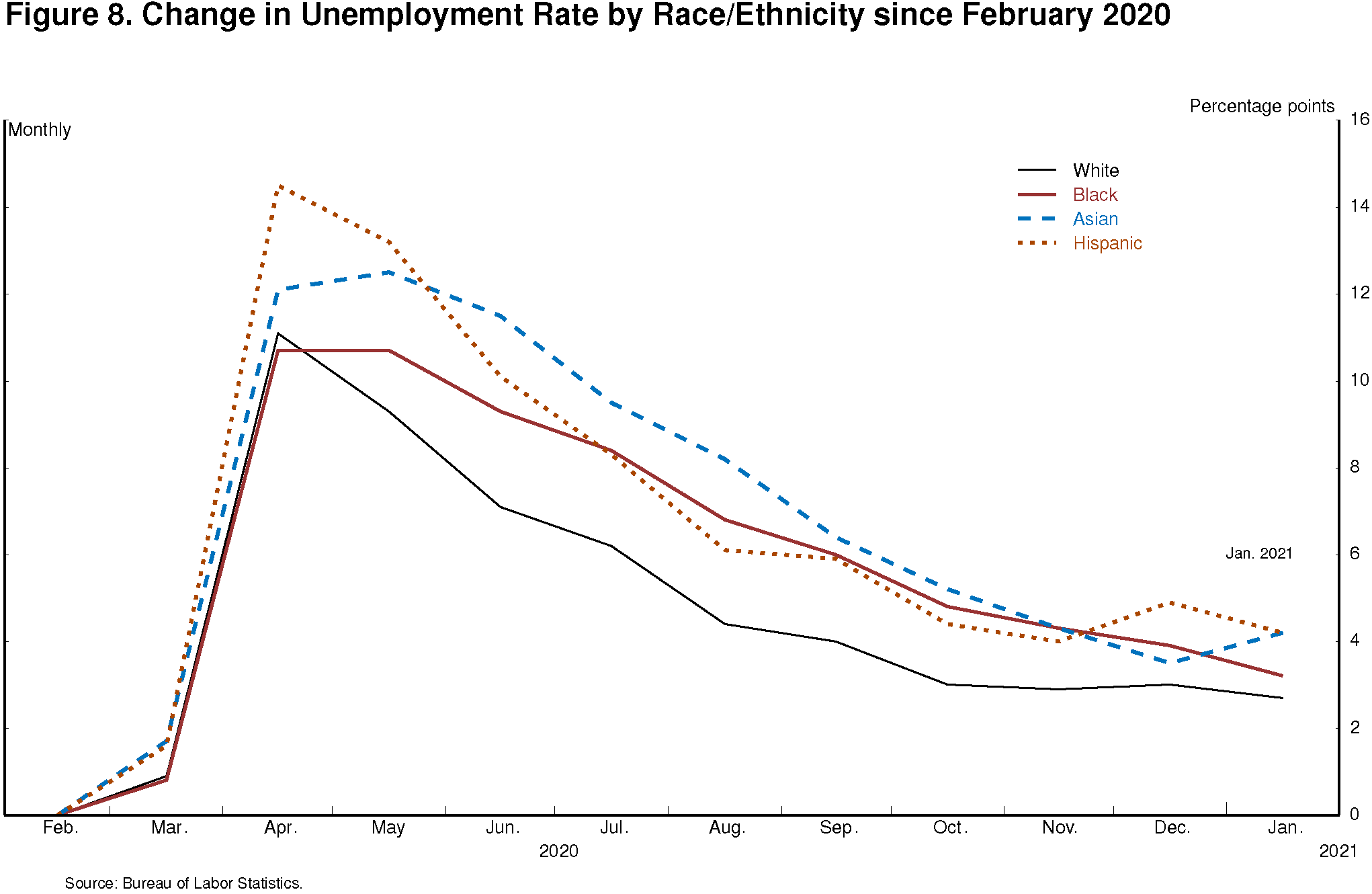

Unfortunately, even those grim statistics understate the decline in labor market conditions for the most economically vulnerable Americans. Aggregate employment has declined 6.5 percent since last February, but the decline in employment for workers in the top quartile of the wage distribution has been only 4 percent, while the decline for the bottom quartile has been a staggering 17 percent (figure 7). Moreover, employment for these workers has changed little in recent months, while employment for the higher-wage groups has continued to improve. Similarly, the unemployment rates for Blacks and Hispanics have risen significantly more than for whites since February 2020 (figure 8). As a result, economic disparities that were already too wide have widened further.

{kind=link}

{kind=link}

In the past few months, improvement in labor market conditions stalled as the rate of infections sharply increased. In particular, jobs in the leisure and hospitality sector dropped over 1/2 million in December and a further 61,000 in January. The recovery continues to depend on controlling the spread of the virus, which will require mass vaccinations in addition to continued vigilance in social distancing and mask wearing in the meantime.

Since the onset of the pandemic, we have been concerned about its longer-term effects on the labor market. Extended periods of unemployment can inflict persistent damage on lives and livelihoods while also eroding the productive capacity of the economy.6 And we know from the previous expansion that it can take many years to reverse the damage.

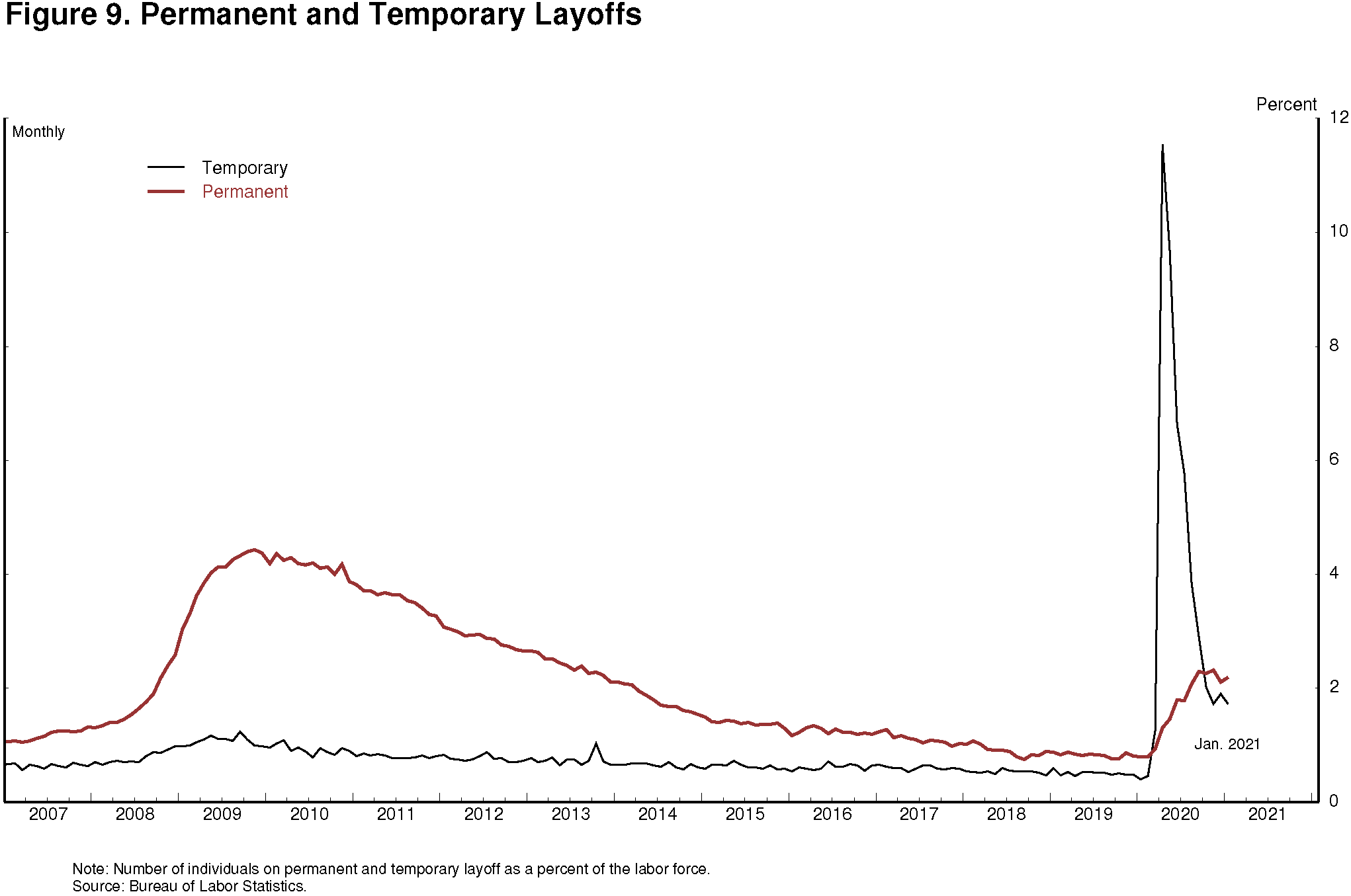

At the start of the pandemic, the increase in unemployment was almost entirely due to temporary job losses.7 Temporarily laid-off workers tend to return to work much more quickly, on average, than those whose ties to their former employers are permanently severed. But as some sectors of the economy have continued to struggle, permanent job loss has increased (figure 9). So too has long-term unemployment. Still, as of January, the level of permanent job loss, as a fraction of the labor force, was considerably smaller than during the Great Recession. Research shows that the Paycheck Protection Program has played an important role in limiting permanent layoffs and preserving small businesses.8 The renewal of the program this year in the face of another surge in COVID-related job cuts is an encouraging development.

{kind=link}

Of course, in a healthy market-based economy, perpetual churn will always render some jobs obsolete as they are replaced by new employment opportunities. Over time, workers and capital move from firm to firm and from sector to sector. It is likely that the pandemic has both increased the need for such movements and brought forward some movement that would have occurred eventually.9

More Articles

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Board of Governors: Minutes of the Federal Open Market Committee June 14–15, 2022; Consumer Price Inflation Remained Elevated

- Federal Reserve issues FOMC statement; Overall Economic Activity, Job Gains and Inflation: "The Committee is strongly committed to returning inflation to its 2 percent objective."

- "Operating Under A Cloud of Uncertainty": Janet Yellen's FOMC Press Conference About Raising the Target Range for Federal Funds Rate to 1/2 to 3/4 %

- Ben Speaks: The Economic Outlook and Monetary and Fiscal Policy