Federal Reserve Chair Jerome H. Powell: Getting Back to a Strong Labor Market

February 10, 2021

Getting Back to a Strong Labor Market

Chair Jerome H. Powell At the Economic Club of New York (via webcast)

The Labor Market of a Year Ago

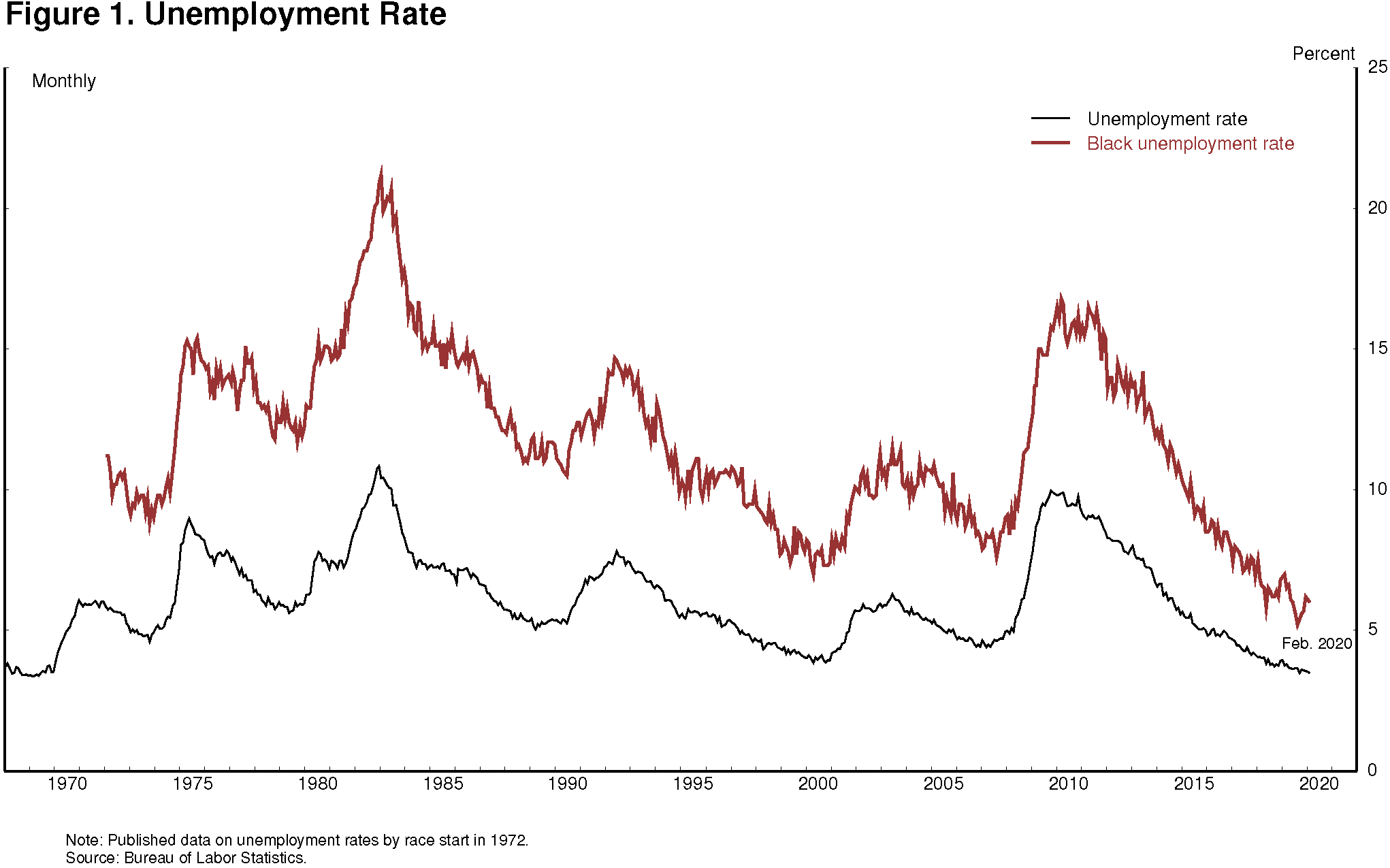

We need only look to February of last year to see how beneficial a strong labor market can be. The overall unemployment rate was 3.5 percent, the lowest level in a half-century. The unemployment rate for African Americans had also reached historical lows (figure 1). Prime-age labor force participation was the highest in over a decade, and a high proportion of households saw jobs as "plentiful."1 Overall wage growth was moderate, but wages were rising more rapidly for earners on the lower end of the scale. These encouraging statistics were reaffirmed and given voice by those we met and conferred with, including the community, labor, and business leaders; retirees; students; and others we met with during the 14 Fed Listens events we conducted in 2019.2

{kind=link}

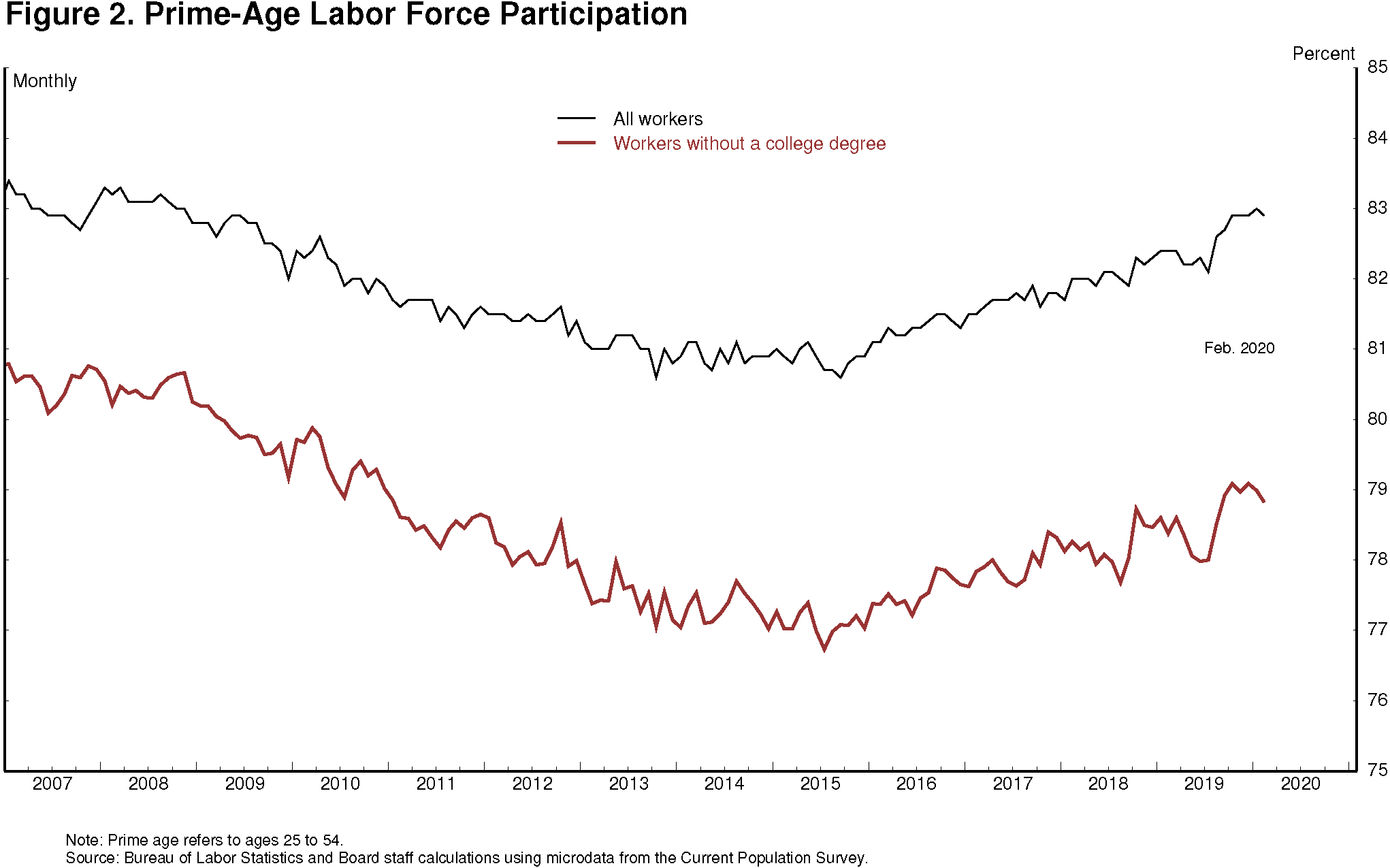

Many of these gains had emerged only in the later years of the expansion. The labor force participation rate, for example, had been steadily declining from 2008 to 2015 even as the recovery from the Global Financial Crisis unfolded. In fact, in 2015, prime-age labor force participation — which I focus on because it is not significantly affected by the aging of the population — reached its lowest level in 30 years even as the unemployment rate declined to a relatively low 5 percent. Also concerning was that much of the decline in participation up to that point had been concentrated in the population without a college degree (figure 2). At the time, many forecasters worried that globalization and technological change might have permanently reduced job opportunities for these individuals, and that, as a result, there might be limited scope for participation to recover.

{kind=link}

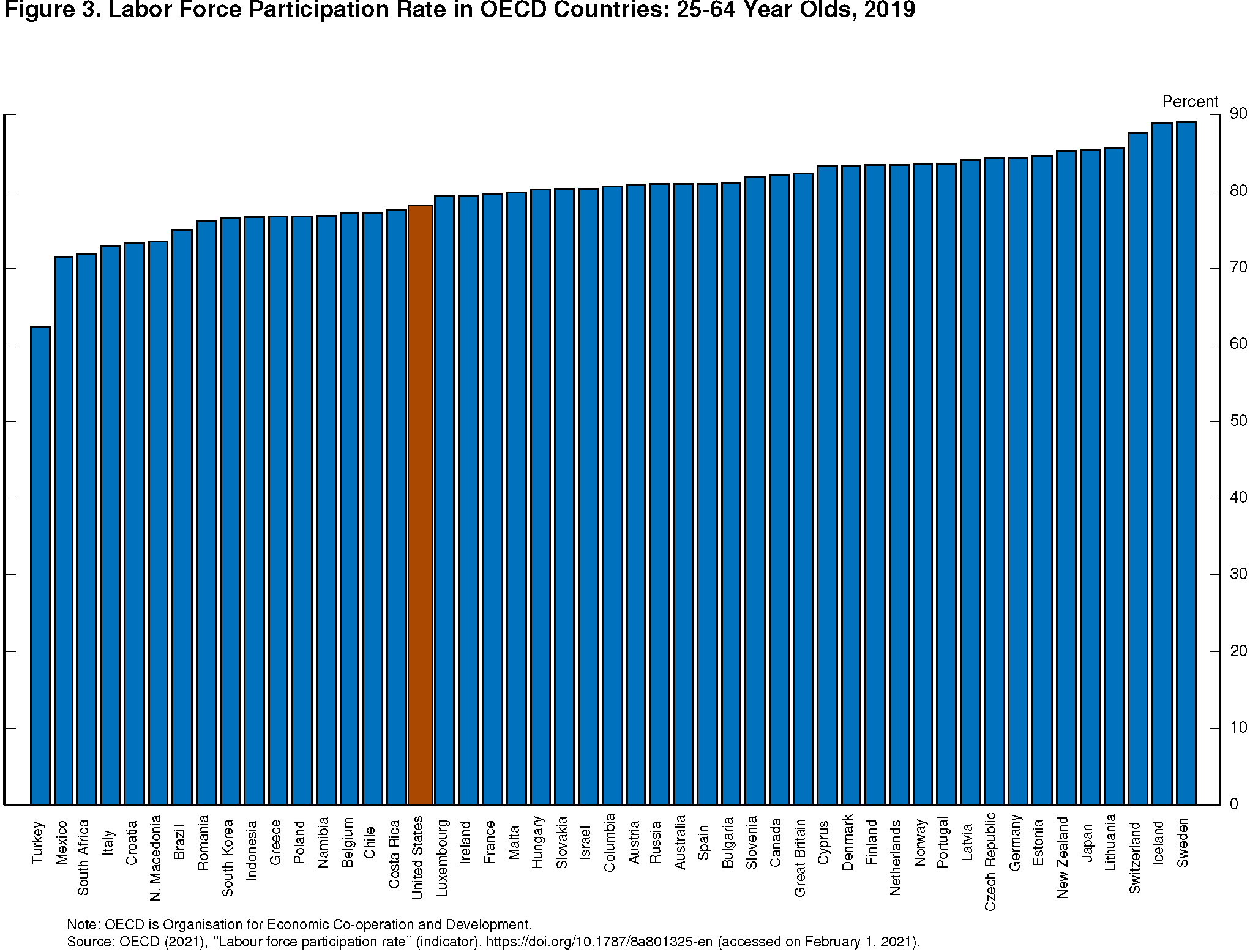

Fortunately, the participation rate after 2015 consistently outperformed expectations, and by the beginning of 2020, the prime-age participation rate had fully reversed its decline from the 2008-to-2015 period. Moreover, gains in participation were concentrated among people without a college degree. Given that U.S. labor force participation has lagged relative to other advanced economy nations, this progress was especially welcome (figure 3).3

{kind=link}

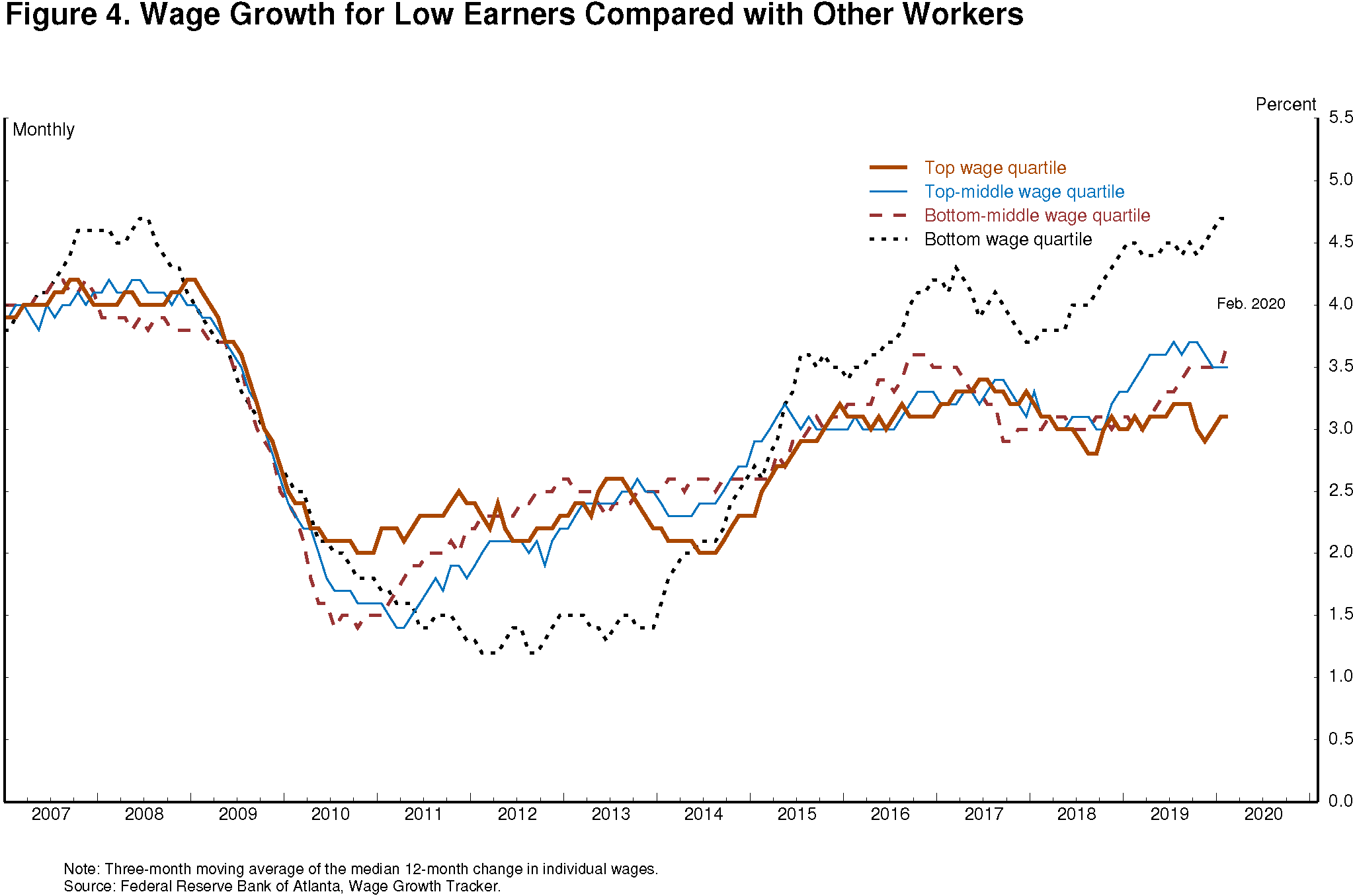

As I mentioned, we also saw faster wage growth for low earners once the labor market had strengthened sufficiently. Nearly six years into the recovery, wage growth for the lowest earning quartile had been persistently modest and well below the pace enjoyed by other workers. At the tipping point of 2015, however, as the labor market continued to strengthen, the trend reversed, with wage growth for the lowest quartile consistently and significantly exceeding that of other workers (figure 4).

{kind=link}

At the end of 2015, the Black unemployment rate was still quite elevated, at 9 percent, despite the relatively low overall unemployment rate. But that disparity too began to shrink; as the expansion continued beyond 2015, Black unemployment reached a historic low of 5.2 percent, and the gap between Black and white unemployment rates was the narrowest since 1972, when data on unemployment by race started to be collected. Black unemployment has tended to rise more than overall unemployment in recessions but also to fall more quickly in expansions.4 Over the course of a long expansion, these persistent disparities can decline significantly, but, without policies to address their underlying causes, they may increase again when the economy ultimately turns down.

More Articles

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Board of Governors: Minutes of the Federal Open Market Committee June 14–15, 2022; Consumer Price Inflation Remained Elevated

- Federal Reserve issues FOMC statement; Overall Economic Activity, Job Gains and Inflation: "The Committee is strongly committed to returning inflation to its 2 percent objective."

- "Operating Under A Cloud of Uncertainty": Janet Yellen's FOMC Press Conference About Raising the Target Range for Federal Funds Rate to 1/2 to 3/4 %

- Ben Speaks: The Economic Outlook and Monetary and Fiscal Policy