With vaccinations rising, schools reopening, and enhanced unemployment benefits ending, some factors that may be holding back job seekers are likely fading.6 While the Delta variant presents a near-term risk, the prospects are good for continued progress toward maximum employment.

{kind=link}

The Path Ahead: Inflation

The rapid reopening of the economy has brought a sharp run-up in inflation. Over the 12 months through July, measures of headline and core personal consumption expenditures inflation have run at 4.2 percent and 3.6 percent, respectively — well above our 2 percent longer-run objective.7 Businesses and consumers widely report upward pressure on prices and wages. Inflation at these levels is, of course, a cause for concern. But that concern is tempered by a number of factors that suggest that these elevated readings are likely to prove temporary. This assessment is a critical and ongoing one, and we are carefully monitoring incoming data.

The dynamics of inflation are complex, and we assess the inflation outlook from a number of different perspectives, as I will now discuss.

1. The absence so far of broad-based inflation pressures

The spike in inflation is so far largely the product of a relatively narrow group of goods and services that have been directly affected by the pandemic and the reopening of the economy. Durable goods alone contributed about 1 percentage point to the latest 12‑month measures of headline and core inflation. Energy prices, which rebounded with the strong recovery, added another 0.8 percentage point to headline inflation, and from long experience we expect the inflation effects of these increases to be transitory. In addition, some prices—for example, for hotel rooms and airplane tickets—declined sharply during the recession and have now moved back up close to pre-pandemic levels. The 12-month window we use in computing inflation now captures the rebound in prices but not the initial decline, temporarily elevating reported inflation. These effects, which are adding a few tenths to measured inflation, should wash out over time.

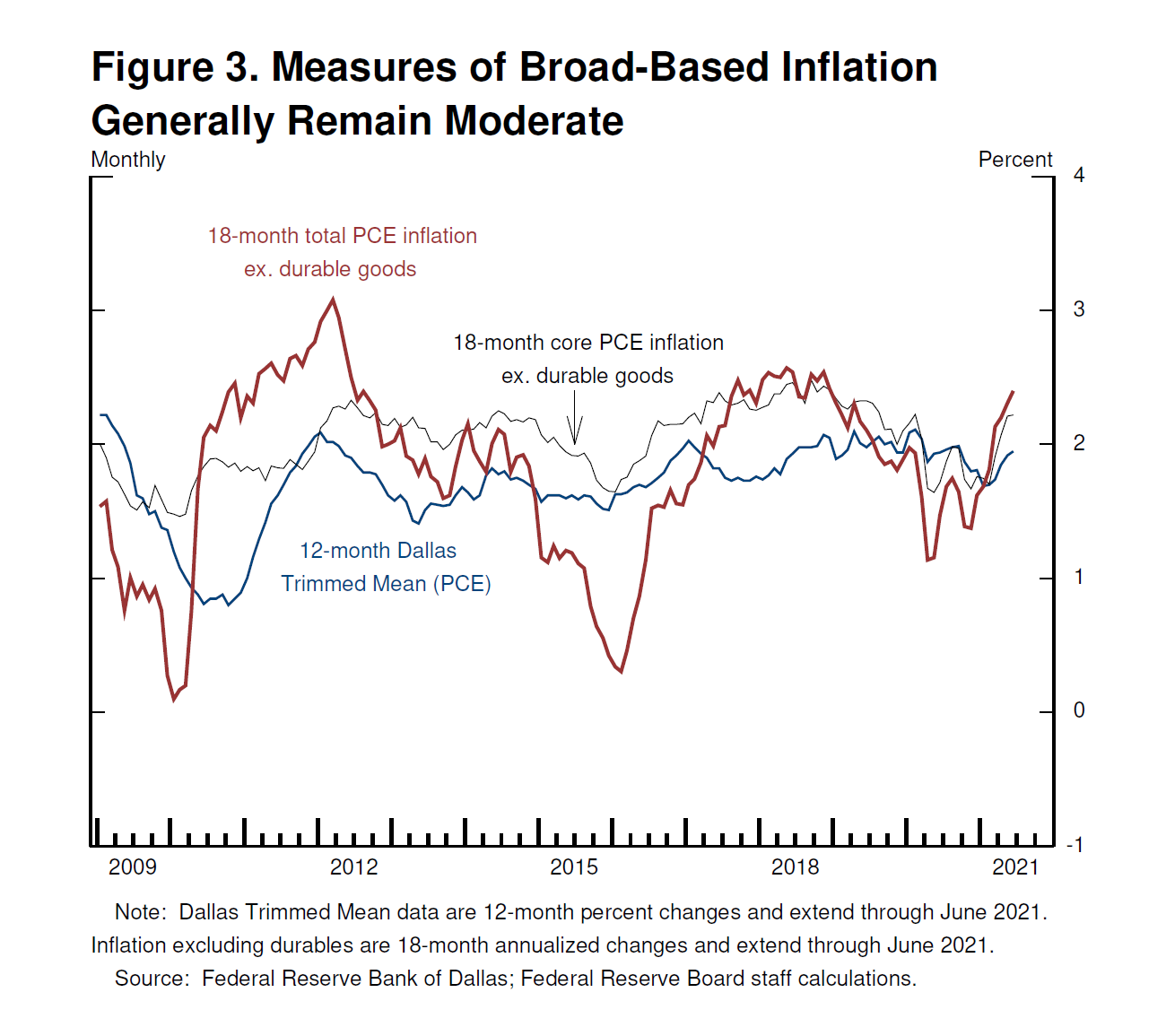

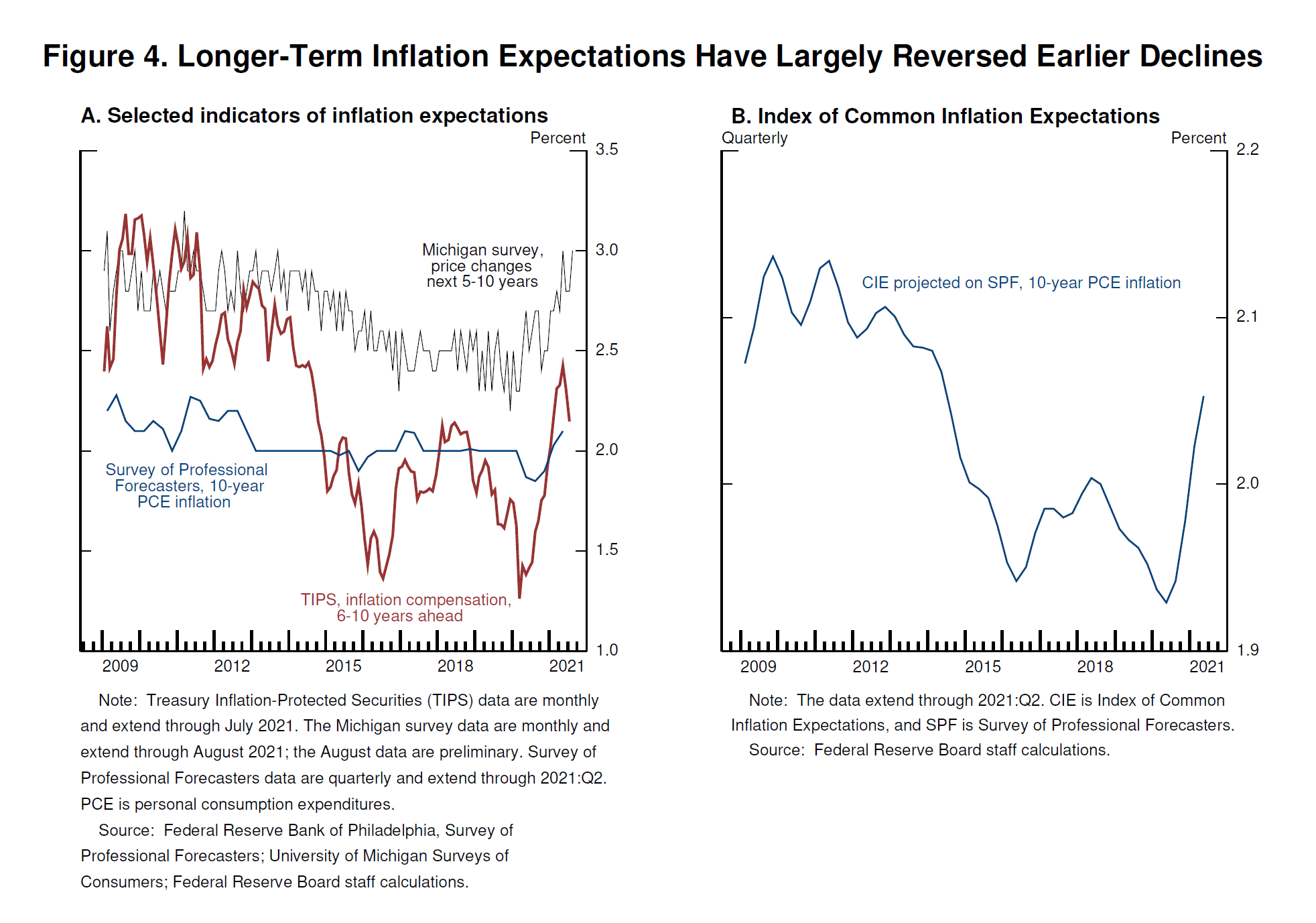

We consult a range of measures meant to capture whether price increases for particular items are spilling over into broad-based inflation. These include trimmed mean measures and measures excluding durables and computed from just before the pandemic. These measures generally show inflation at or close to our 2 percent longer-run objective (figure 4). We would be concerned at signs that inflationary pressures were spreading more broadly through the economy.

{kind=link}

2. Moderating inflation in higher-inflation items

We are also directly monitoring the prices of particular goods and services most affected by the pandemic and the reopening, and are beginning to see a moderation in some cases as shortages ease. Used car prices, for example, appear to have stabilized; indeed, some price indicators are beginning to fall. If that continues, as many analysts predict, then used car prices will soon be pulling measured inflation down, as they did for much of the past decade.8

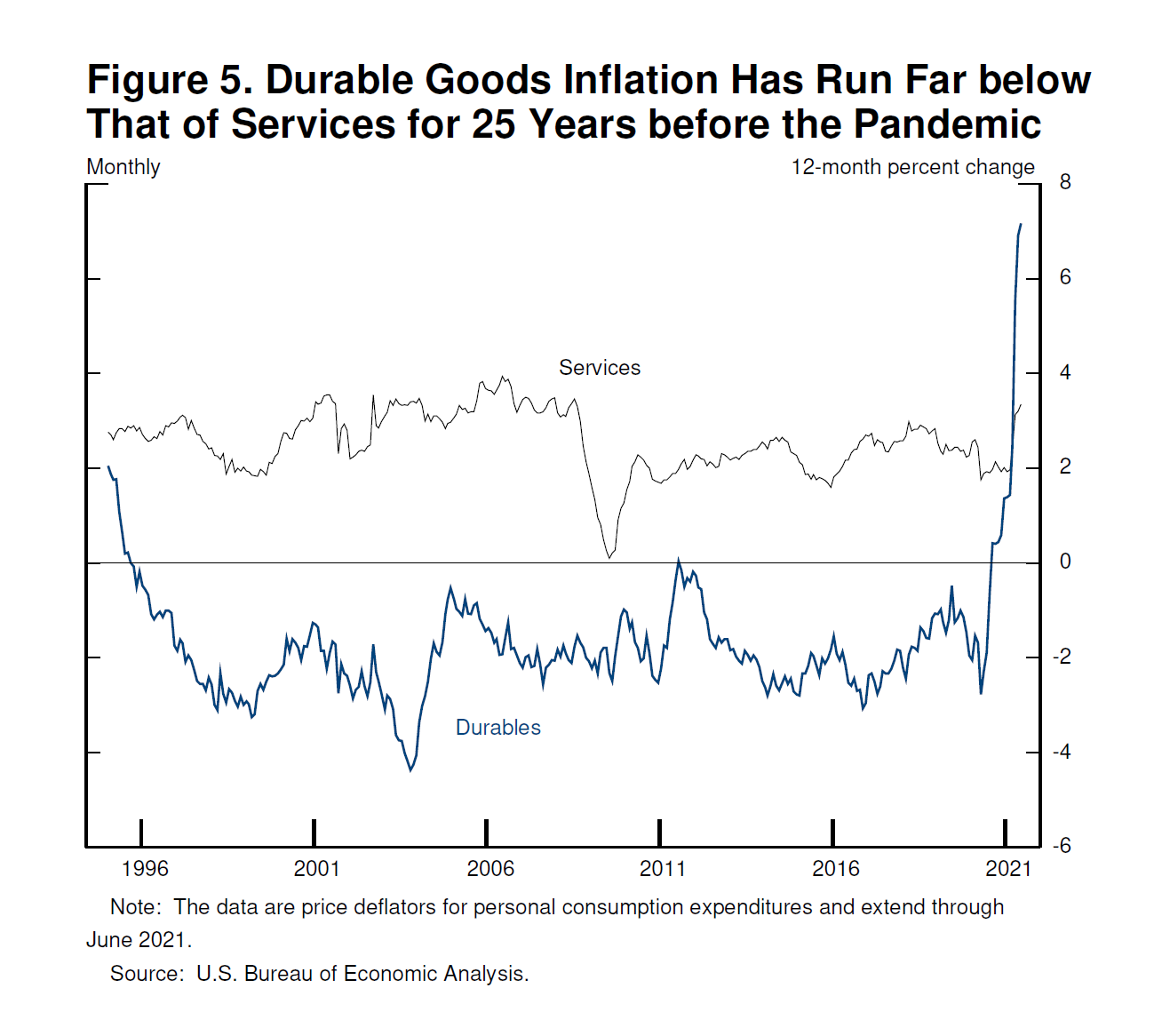

This same dynamic of upward inflation pressure dissipating and, in some cases, reversing seems likely to play out in durables more generally. Over the 25 years preceding the pandemic, durables prices actually declined, with inflation averaging negative 1.9 percent per year (figure 5).9 As supply problems have begun to resolve, inflation in durable goods other than autos has now slowed and may be starting to fall. It seems unlikely that durables inflation will continue to contribute importantly over time to overall inflation. We will be looking for evidence that supports or undercuts that expectation.

{kind=link}

3. Wages

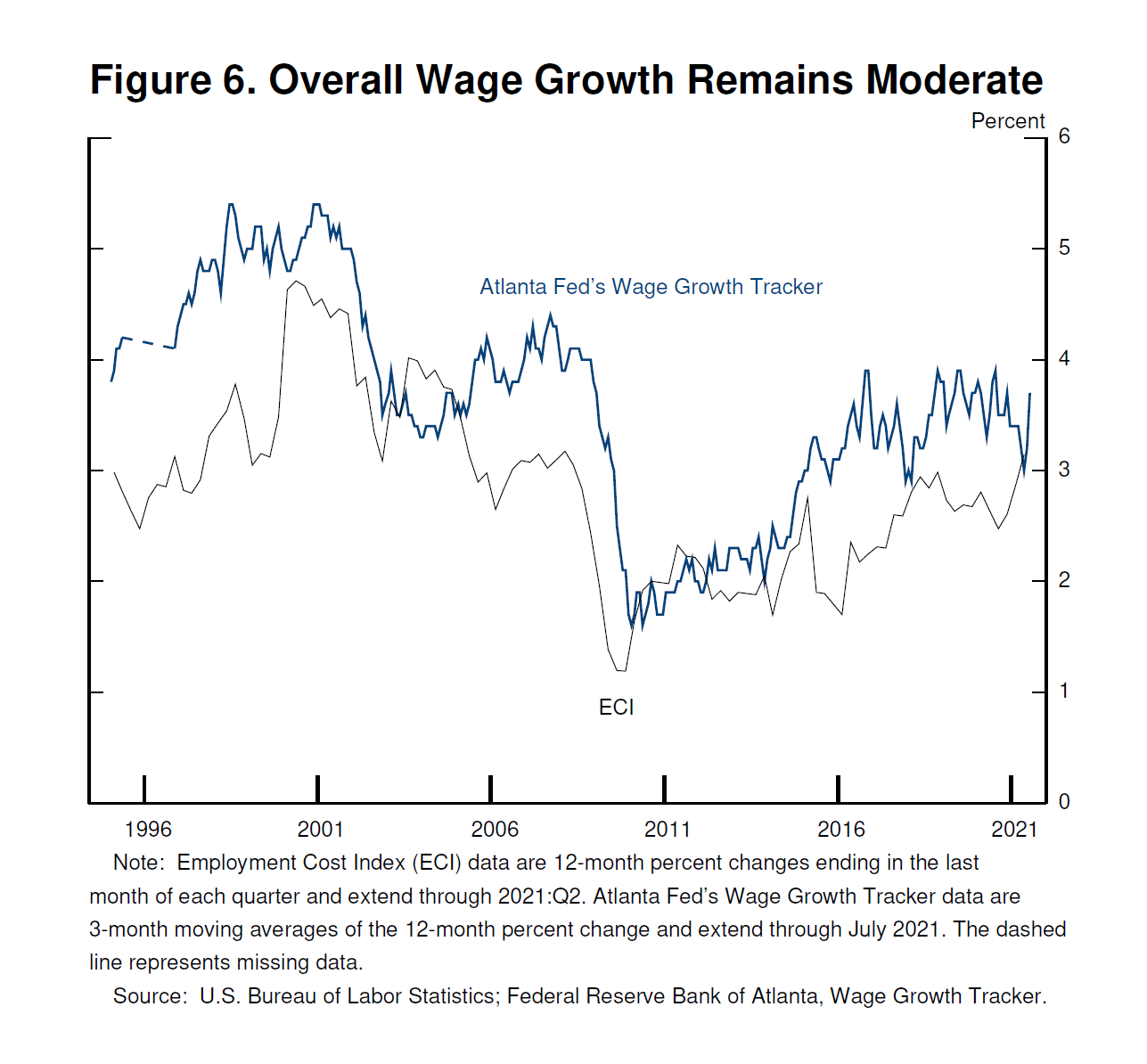

We also assess whether wage increases are consistent with 2 percent inflation over time. Wage increases are essential to support a rising standard of living and are generally, of course, a welcome development. But if wage increases were to move materially and persistently above the levels of productivity gains and inflation, businesses would likely pass those increases on to customers, a process that could become the sort of "wage–price spiral" seen at times in the past.10 Today we see little evidence of wage increases that might threaten excessive inflation (figure 6). Broad-based measures of wages that adjust for compositional changes in the labor force, such as the employment cost index and the Atlanta Wage Growth Tracker, show wages moving up at a pace that appears consistent with our longer-term inflation objective. We will continue to monitor this carefully.

{kind=link}

4. Longer-term inflation expectations

Policymakers and analysts generally believe that, as long as longer-term inflation expectations remain anchored, policy can and should look through temporary swings in inflation. Our monetary policy framework emphasizes that anchoring longer-term expectations at 2 percent is important for both maximum employment and price stability.

We carefully monitor a wide range of indicators of longer-term inflation expectations. These measures today are at levels broadly consistent with our 2 percent objective (figure 4). Because measures of inflation expectations are individually noisy, we also focus on common patterns across the measures. One approach to summarizing these patterns is the Board staff's index of common inflation expectations (CIE), which combines information from a broad range of survey and market-based measures.11 This index captures a general move down in expectations starting around 2014, a time when inflation was running persistently below 2 percent. More recently, the index shows a welcome reversal of that decline and is now at levels more consistent with our 2 percent objective.

Longer-term inflation expectations have moved much less than actual inflation or near-term expectations, suggesting that households, businesses, and market participants also believe that current high inflation readings are likely to prove transitory and that, in any case, the Fed will keep inflation close to our 2 percent objective over time.12

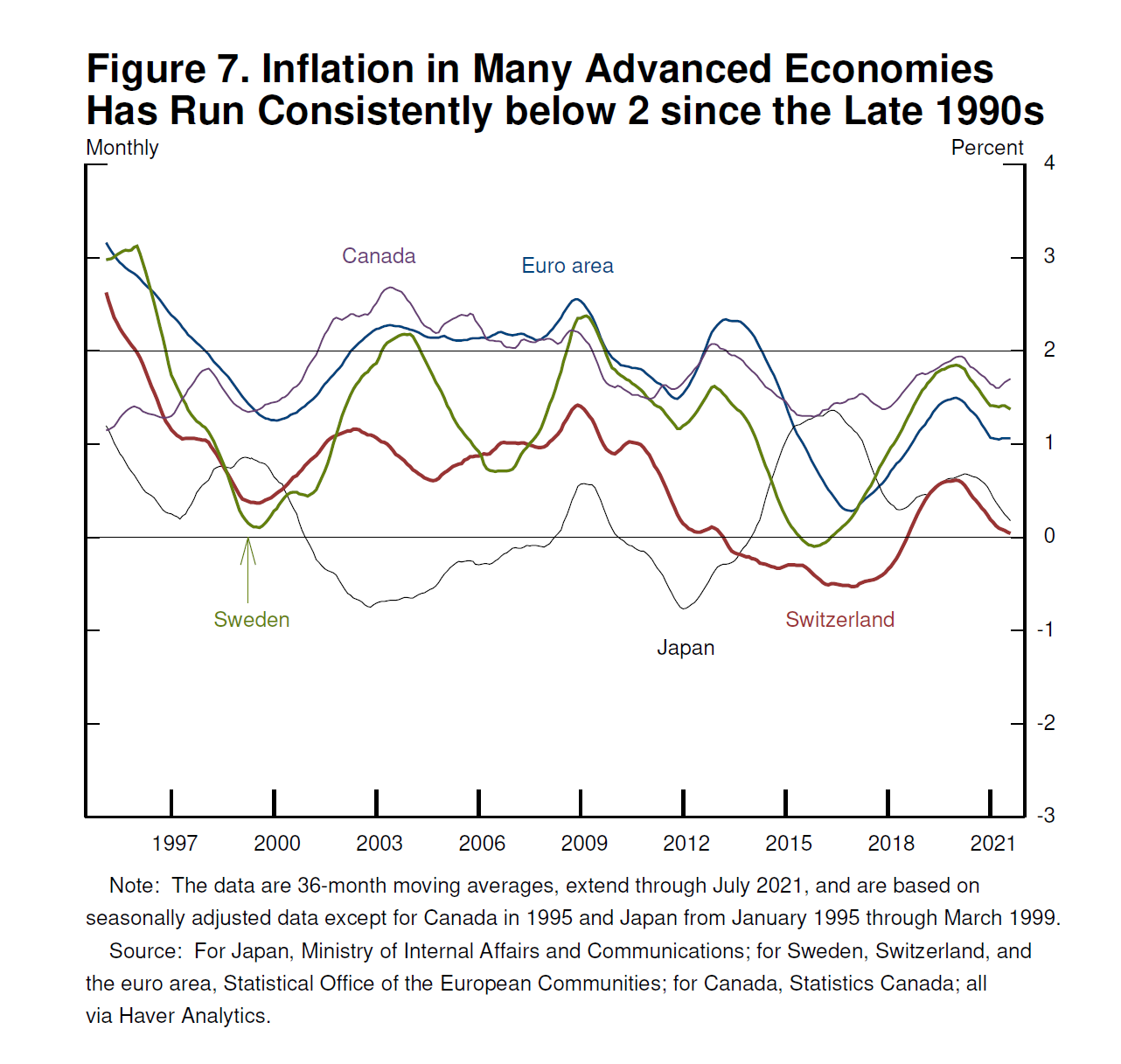

5. The prevalence of global disinflationary forces over the past quarter century

Finally, it is worth noting that, since the 1990s, inflation in many advanced economies has run somewhat below 2 percent even in good times (figure 7). The pattern of low inflation likely reflects sustained disinflationary forces, including technology, globalization and perhaps demographic factors, as well as a stronger and more successful commitment by central banks to maintain price stability.13 In the United States, unemployment ran below 4 percent for about two years before the pandemic, while inflation ran at or below 2 percent. Wages did move up across the income spectrum—a welcome development—but not by enough to lift price inflation consistently to 2 percent. While the underlying global disinflationary factors are likely to evolve over time, there is little reason to think that they have suddenly reversed or abated. It seems more likely that they will continue to weigh on inflation as the pandemic passes into history.14

{kind=link}

We will continue to monitor incoming inflation data against each of these assessments.

More Articles

- Chair Jerome H. Powell Remarks at the Stanford Business, Government and Society Forum

- 2024 Tax Filing Season Set for January 29; IRS Continues to Make Improvements to Help Taxpayers

- November 1, 2023 Chair Jerome Powell’s Press Conference on Employment and Inflation

- Board of Governors of the Federal Reserve System: Something’s Got to Give by Governor Christopher J. Waller

- Brief Remarks on the Economy and Monetary Policy Governor Michelle W. Bowman At the 2023 CEO and Senior Management Summit and Annual Meeting, sponsored by the Kansas Bankers Association, Colorado Springs, Colorado

- Jerome Powell's Semiannual Monetary Policy Report; Strong Wage Growth; Inflation, Labor Market, Unemployment, Job Gains, 2 Percent Inflation

- February’s Hot Data Releases: Governor Christopher J. Waller, Federal Reserve Board Frames a Few of the Issues Around Inflation and the Economic Outlook

- Congressional Budget Office: Federal Budget Deficit Totals $1.4 Trillion in 2023; Annual Deficits Average $2.0 Trillion Over the 2024–2033 Period

- Remarks by Secretary of the Treasury Janet L. Yellen at the Bureau of Engraving and Printing Facility in Fort Worth, Texas

- The Beige Book Summary of Commentary on Current Economic Conditions By Federal Reserve District Wednesday November 30, 2022